French Bank Account Requirements: 2026 Expat Guide

Navigating French bank account requirements? Our 2026 guide for expats & non-residents covers IDs, income proof, and how to open an account for property.

published

Outrank AI

bank account requirements, open account in france, expat mortgage france, non-resident bank account, french property purchase

81d73c17-f775-4a6d-9138-69117730af95

You've agreed a price on a flat in Paris or a house in the Alps. The notaire is moving, the seller wants reassurance, and your mortgage file is nearly ready. Then the bank asks for something that sounds simple and turns out not to be simple at all: a French current account.

For a non-resident, this is often the first real administrative blockage. Not because banks are trying to be difficult, but because the account is tied to identity checks, source-of-funds checks, future mortgage payments, insurance debits, and the final transfer at completion. If the account opening drags, the whole property timeline can drag with it.

In practice, a French bank account is rarely just a convenience for an expat buyer. It often becomes the operational base of the purchase. The mortgage lender wants to see how money will circulate, where the deposit comes from, and whether monthly repayments can be managed cleanly from an account they can monitor and service.

The First Hurdle to Your French Property Dream

The frustrating part is that many buyers arrive at this stage thinking the hard part was finding the property. It usually isn't. The hard part is packaging yourself into a file that a French compliance team can approve without hesitation.

French banks don't look at a non-resident account opening the way a retail bank might look at a routine domestic application. They see extra compliance questions immediately. Where do you live? Where are you taxed? Where is your income earned? Is the property for personal use, rental use, or long-term investment? Are funds coming from salary, dividends, retained company earnings, or an asset sale?

Why the account matters so early

For a property purchase, the account often sits at the center of several moving parts:

Deposit management: The bank may want the account open before larger transfers begin.

Mortgage administration: Loan disbursement and monthly repayments need a clean route.

Proof of seriousness: A complete account-opening file can strengthen your broader banking relationship.

Compliance continuity: The same documents often feed both the account review and the mortgage review.

Practical rule: Treat the bank account as part of the mortgage application, not as a separate admin task.

Many buyers lose time because they approach the wrong bank first, send incomplete documents, or assume a foreign tax number or overseas address will automatically cause refusal. That isn't how it works. The issue is whether your file answers the bank's questions clearly enough, in the format the bank expects.

A clean, well-prepared file can move. A vague one stalls.

Understanding Universal Bank Account Requirements

Before dealing with French specifics, it helps to understand the logic behind bank account requirements everywhere. Banks are building a verified identity stack. They need to know who you are, where you live, how you're identified for tax purposes, and whether the money entering the account has a coherent origin.

Your financial passport

In most cases, the file starts with three core pillars.

Proof of identity

A valid passport is usually the strongest document for an international client. Some banks may also accept another government-issued photo ID, but passport-based files tend to travel best across borders.Proof of residential address

This doesn't have to be French at the start. It has to be current, legible, and consistent with the rest of your file. If your passport says one country, your tax documents show another, and your bank statements show a third address, expect questions.Proof of tax status

Banks commonly ask for a taxpayer or identification number. The broader rule is not “must have one specific domestic number.” The broader rule is “must provide a valid government identification number appropriate to your status.”

The U.S. Consumer Financial Protection Bureau states that you do not need a Social Security number to get a bank or credit union account, and that banks may accept an ITIN, passport number with country of issuance, alien ID number, or another government-issued ID number, depending on the case and the institution's requirements (CFPB guidance on bank accounts).

Why banks insist on these documents

This is the KYC and AML layer. Know Your Customer and anti-money laundering controls are not side issues. They are the file.

A bank doesn't just want to see your name. It wants to reconcile identity, residence, tax status, and expected account activity. For a French property buyer, that often means the account-opening team wants enough information to understand not only who you are, but why this account is being opened now, what transactions are expected, and whether a later mortgage relationship is plausible.

If a document is genuine but doesn't fit the bank's internal logic, the file can still stall.

What works in practice

The strongest files are consistent across documents. The name format matches. Addresses line up. Tax residence is clear. Bank statements are easy to read. If your statements are cluttered, poorly scanned, or missing pages, clean presentation matters. For buyers assembling a mortgage-ready file, OkraPDF's approach to bank statements is a useful reference for how to standardize statements into something easier to review and share.

A simple working checklist at this stage looks like this:

Identity document ready: Passport valid, readable, and not close to expiry.

Address evidence current: Utility bill, bank statement, or official correspondence that matches your declared residence.

Tax identifier available: Home-country tax number or equivalent government identifier.

Name consistency checked: Same spelling, same sequence, same middle names where relevant.

That basic discipline solves more account-opening problems than one might expect.

Navigating French Requirements for Non-Residents

French bank account requirements become more demanding when you don't yet have a French footprint. That's where generic advice stops being useful. A local salaried employee with a French payslip, French tax number, and EDF bill is easy for the bank to place. A British buyer living in Dubai, or an American couple buying through future relocation plans, is not.

When you don't have French proof of address

This is the most common friction point. Buyers are often told they need a French utility bill, then assume the process is impossible until after completion. That's too simplistic.

A more useful distinction is this: mandatory compliance checks are one thing, bank-specific onboarding preferences are another. For people without a local footprint, alternative documents can help bridge the gap. The key issue is understanding which documents are compulsory and which ones are merely the bank's preferred format. That distinction is highlighted in public discussion of account access for newly arrived migrants and cross-border workers, including the role of alternatives such as an employment contract or property purchase agreement when standard residency proof is missing (analysis of onboarding barriers and alternative documents).

In French property files, the following often help:

Compromis de vente: Shows a genuine pending purchase in France.

Attestation from the seller or notaire: Useful where the future address is known but occupancy hasn't started.

Foreign proof of residence: Still important, even when the property being bought is in France.

Explanatory cover note: Briefly clarifies your status, timeline, and expected account use.

Presenting foreign income so a French bank can read it

Many non-residents often lose credibility without realizing it at this stage. The problem isn't always the income itself. It's the way it is presented.

French retail banking teams understand salary best when it looks like salary. They understand company income best when company and personal flows are separated cleanly. They struggle when buyers submit mixed personal and business transactions, incomplete statements, or unexplained inbound transfers.

A practical file for foreign income usually works better when it includes:

Document type | What the bank wants to understand |

|---|---|

Payslips or salary certificates | Stability and employer identity |

Personal bank statements | Net income landing pattern and spending profile |

Tax returns | Broader income consistency |

Company accounts or dividend documents | Source of business-owner income |

Asset sale evidence | Origin of one-off funds used for deposit |

If you hold investment assets abroad, tax treatment can also become part of the wider conversation, especially where income streams support affordability. For that reason, clients with portfolios often need to understand how French lenders will view foreign assets alongside French tax on foreign securities.

Banks are more comfortable with complicated income than with unexplained income.

Translation and formalization

Not every foreign document needs sworn translation. Some banks will accept English-language financial documents, especially if the structure is familiar and the figures are easy to follow. Others will insist on French translation for tax returns, company documents, or legal papers.

What matters is not translating everything blindly. It's translating the documents that create decision friction. In practice, those are usually the papers that establish legal status, ownership, or unusual income mechanics.

Use this order of priority:

Translate first: Civil-status documents, legal company documents, unusual income support.

Ask before translating: Standard bank statements, straightforward payslips, common tax summaries.

Formalize if needed: Apostille or notarization where the bank or notaire specifically asks for it.

That saves both time and money, which matters when your mortgage timeline is already running.

Accounts for Property Investment Vehicles like an SCI

Buying through an SCI changes the file completely. The bank is no longer opening an account only for an individual customer. It is onboarding a legal structure, then checking the people behind it.

What the bank reviews in an SCI file

For business accounts, banks have to verify both the entity and the individuals who control it. Public guidance on business banking makes the broader point clearly: registered entities typically need a business tax ID and official formation papers so the bank can satisfy KYC and AML requirements for the company and its controlling persons (SBA guidance on opening a business bank account).

For a French SCI, that usually means the bank will ask for a package closer to this:

Statuts of the SCI: The governing constitutional document.

Proof of registration: Often the Kbis once available.

Identity documents for each shareholder and manager: Not just for the signatory.

Address evidence for the individuals involved: Especially for non-resident shareholders.

Tax and activity explanation: Why the SCI exists and what property it will hold.

The UBO point that delays files

The Ultimate Beneficial Owner declaration is where many buyers underestimate the work. Banks need to know who ultimately owns or controls the structure. If ownership is split across spouses, children, holding companies, or family branches, the file must still lead to identifiable real persons.

That exercise matters because the bank isn't just checking the SCI as a legal shell. It's checking the humans behind it, their jurisdictions, and their expected source of funds.

A workable SCI file should answer these questions without ambiguity:

Who are the shareholders?

Who signs for the company?

Who benefits economically from the property?

Where do the funds entering the SCI originate?

An SCI account is rarely approved on documents alone. It is approved on clarity.

For buyers still deciding whether an SCI is the right structure, it's worth reviewing l'expertise Invexa sur la SCI before opening the account, because the ownership structure, tax profile, and financing strategy should align from the start.

What works and what doesn't

What works is preparing the SCI file as if the bank has never seen your structure before. Spell out the roles. Provide an ownership diagram if needed. Separate company funds from personal funds. Explain the acquisition purpose.

What doesn't work is assuming the bank will “figure it out” from several legal PDFs in different languages.

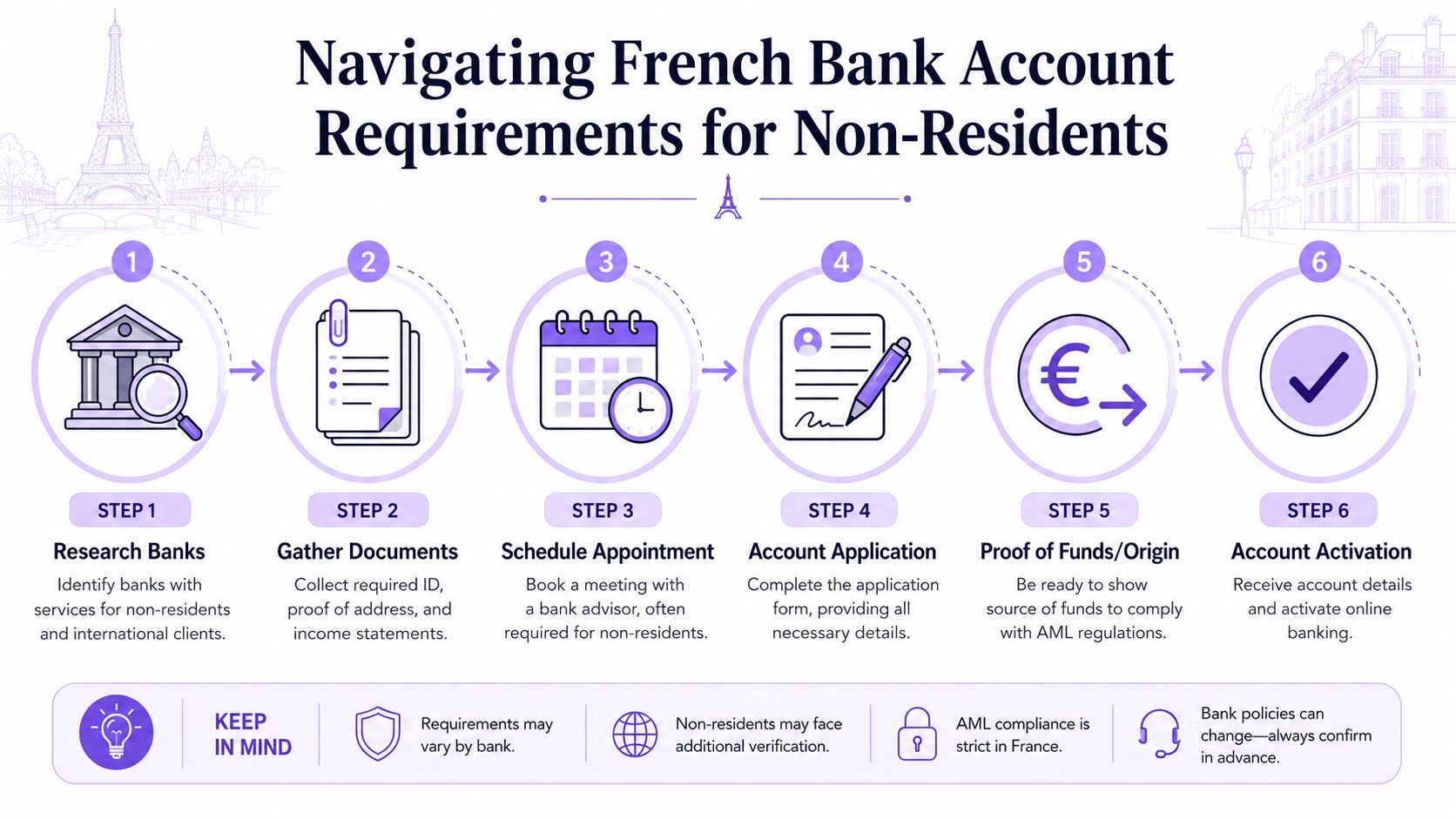

Your Step-by-Step Account Opening Timeline

For non-residents, account opening is rarely instant. The sequence is usually straightforward, but each step can pause if the previous one was handled loosely.

The real order of operations

A practical timeline usually looks like this:

Choose the bank based on your property project

Don't start with branding or app quality. Start with whether the bank handles non-residents, accepts foreign income profiles, and has a mortgage department aligned with your case.Pre-check the document list

Ask for the exact onboarding requirements for your residency status. A bank may accept non-resident clients in theory but require branch-level approval in practice.Submit the file

This may happen remotely, in branch, or through a relationship manager. The strongest submissions include one complete package, not a stream of piecemeal emails.Respond to compliance questions

This stage is normal. Additional questions about source of funds, tax residence, or expected transfers don't mean refusal.Make the opening deposit

Initial funding can be a hard trigger for activation. Consumer guidance notes that minimum opening deposits are common, often in the $25 to $100 range for standard consumer accounts, and that this can determine activation or eligibility for fee waivers and product features (CFPB account-opening checklist).

Where timing usually slips

The first delay comes from document mismatch. The second comes from unexplained money. The third comes from leaving the account opening too close to the mortgage offer stage.

Here is the pattern I see most often:

Stage | Common issue | Better approach |

|---|---|---|

Bank selection | Choosing a bank with no non-resident appetite | Ask about non-resident onboarding before applying |

File submission | Missing pages or unclear scans | Submit one organized PDF set |

Compliance review | Large transfers with no explanation | Provide source-of-funds documents early |

Activation | No initial deposit ready | Pre-position funds before approval |

How to plan around the mortgage

A property purchase has fixed moments. Reservation discussions, compromis signing, mortgage file review, lender approval, notary coordination. The account should be open before it becomes operationally urgent.

That means:

Start early: Ideally before the lender asks for domiciliation or account evidence.

Keep liquidity available: You may need to fund the account quickly once approved.

Use the same narrative everywhere: The account file, mortgage file, and notary file should describe the project the same way.

Open the account when the purchase becomes credible, not when the bank makes it urgent.

If your file is complex, one practical option is to have the banking and financing workstreams coordinated together. That's where a broker such as Invexa can be useful in factual terms, because its work focuses on preparing remote mortgage files for expatriates and non-residents buying in France, which often includes anticipating the account-opening constraints that affect lender acceptance.

Common Pitfalls and Choosing a Mortgage-Friendly Bank

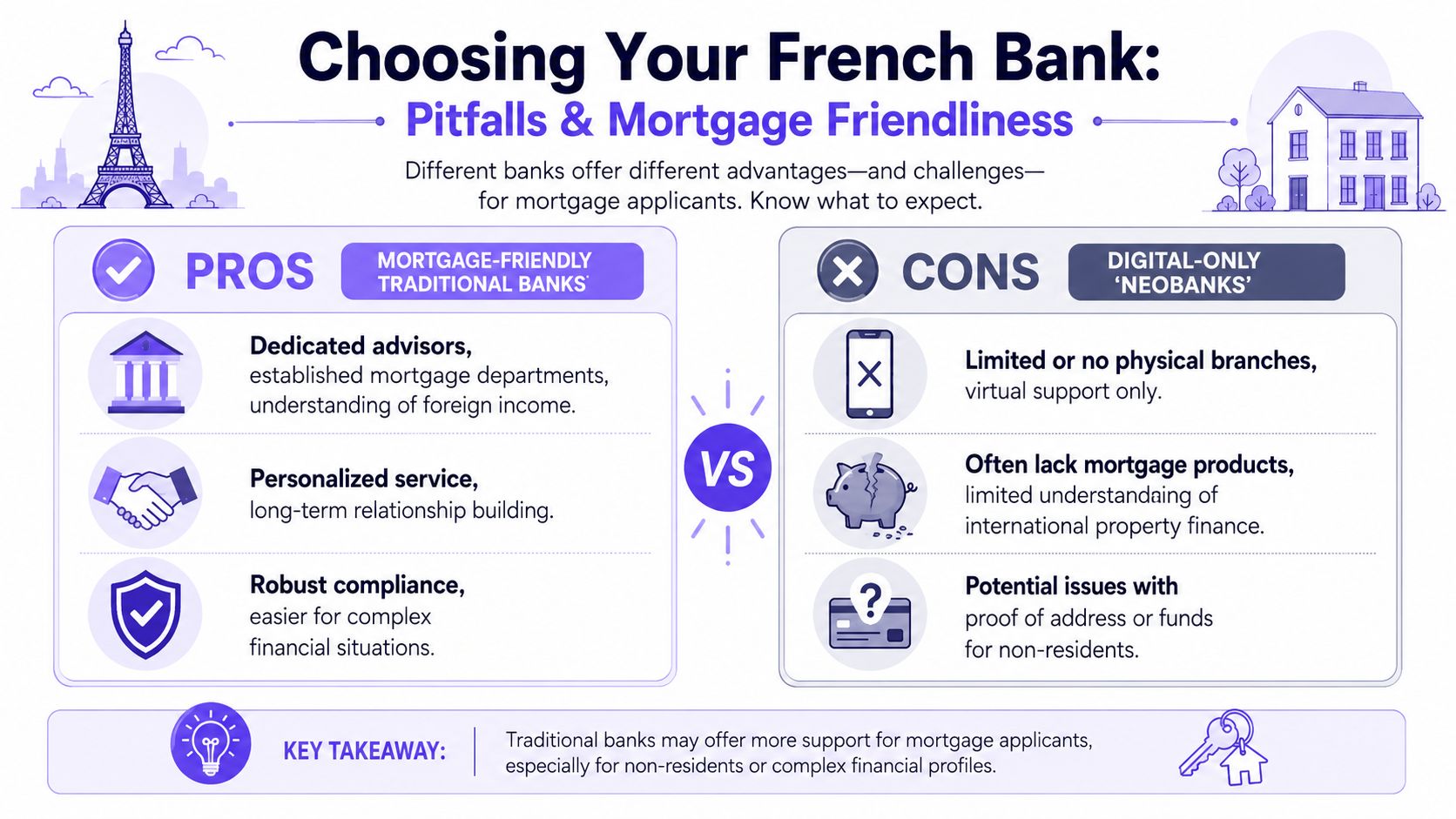

A French bank account for everyday spending and a French bank account that supports a non-resident mortgage are not always the same thing. Buyers often choose the most convenient account, then discover later that the institution isn't set up for the financing side.

The wrong bank can slow the mortgage

Digital-first banks and neobanks can be useful for basic payments. They are often less useful when the project involves property transfers, detailed source-of-funds checks, or a linked mortgage discussion with a human underwriter.

A traditional bank with an established lending arm is usually better placed to handle:

Large incoming transfers linked to a purchase

Foreign income explanation

Coordination with mortgage underwriting

Ongoing account management after loan drawdown

This doesn't mean every branch bank is good for non-residents. Some are excellent. Some are rigid. The point is strategic fit.

Fees matter more than most buyers expect

A cheap-looking account can become expensive if the pricing is opaque. Public analysis of access barriers shows that cost structure remains a major issue. The share of unbanked households citing high or unpredictable fees as a reason rose from 30.8% in 2015 to 35.5% in 2023 (banking access and fee-barrier data).

For an expat buyer, the risk points are practical:

International transfer charges: Relevant when moving deposit funds or topping up monthly.

Maintenance fees: Sometimes modest, sometimes poorly understood at sign-up.

Card and foreign-transaction charges: Important if you'll keep using the account from abroad.

Operational limitations: Some accounts are fine for retail use but awkward for notary-related flows.

What to choose instead

If the account is connected to a mortgage project, choose for capability first, convenience second.

A better decision filter is:

Will this bank lend to my profile, or at least understand it?

Can it handle non-resident compliance without improvisation?

Can it process property-related transactions smoothly?

Are the fees transparent enough for long-term use?

If the purchase depends on financing, your bank choice should support the broader objective of securing a non-resident mortgage France file that can close.

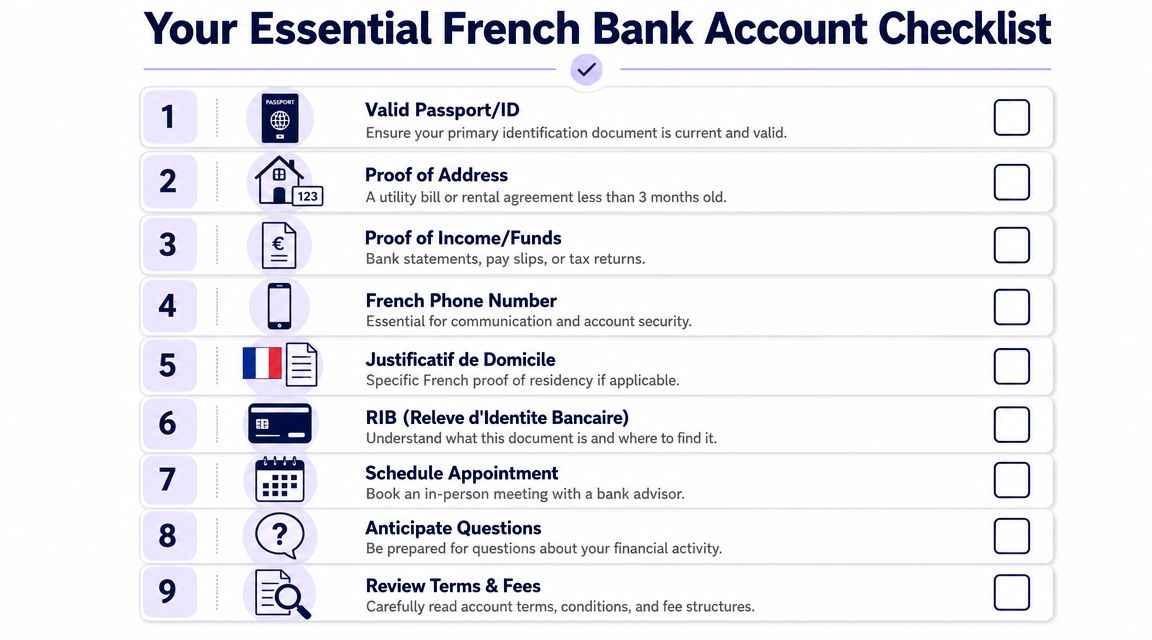

Your Essential French Bank Account Checklist

By the time you apply, the account should feel like an assembled case, not a stack of random documents. That's the difference between a file a bank can process and a file that keeps bouncing back for clarification.

The short checklist that saves time

Valid passport ready: Clear scan, full page, no cropped edges.

Current proof of home address: Foreign address is acceptable if it is current and consistent.

Tax identification details available: Use the number appropriate to your country and status.

Income documents organized: Payslips, tax returns, company documents, or dividend support where relevant.

Source-of-funds evidence prepared: Especially if you'll move a deposit or large savings balance.

French property documents included: Compromis, draft deed material, or notaire references where available.

Phone and contact details stable: Banks dislike changing contact points mid-review.

Fee schedule reviewed: Confirm what you'll pay for transfers, cards, and maintenance.

Mortgage compatibility checked: Make sure the bank account supports the financing plan.

One final practical mindset

If you've financed property in another jurisdiction, don't assume France works the same way. Cross-border buyers often underestimate how closely account opening, compliance, and mortgage underwriting are tied together. That's true in many international markets. Buyers comparing systems sometimes find it helpful to read about other foreign-buyer frameworks, such as understanding Israeli property financing, because it highlights the same recurring issue: lenders want a clear, documentable story.

The good approach is simple. Start early. Over-prepare. Keep every document consistent. Choose the bank for the financing path, not just for the card or the app.

If you're buying property in France from abroad and want a clear view of which banks are likely to work with your profile, Invexa can help you structure the file, align the banking side with the mortgage side, and avoid the delays that usually come from incomplete or badly sequenced documentation.