Understanding Debt to Income Ratio for French Mortgages

Understanding debt to income ratio - Master understanding debt to income ratio for your French mortgage. Discover how banks calculate DTI for expats, what debt

published

Outrank AI

understanding debt to income ratio, dti ratio france, expat mortgage france, french mortgage calculator, improve dti

515a5eaf-5594-4bd0-a61f-bcae5f5481bc

You've found the property. The location is right, the renovation budget seems manageable, and you can already picture the signing at the notaire. Then the bank or broker asks for one number that suddenly controls the entire file: your debt-to-income ratio, or in French banking language, your taux d'endettement.

For expats and non-residents, that moment is often where confidence drops. Your income may be strong, but it's paid in another currency. Your bonus may be regular, but not fully fixed. You may already own property abroad, hold debt in another jurisdiction, or plan to buy through an SCI. A French bank won't read that profile the same way it reads a standard domestic salary file.

That's why understanding debt to income ratio matters so much before you apply. If you know how the ratio is assessed, which debts count, and how your foreign income is interpreted, you can shape the file properly instead of discovering problems halfway through underwriting. If you want a first estimate before speaking to a lender, a good starting point is to calculer son prêt immobilier expat.

Your Dream French Property and the DTI Hurdle

A typical non-resident buyer starts with the wrong question. They ask, “How much can I borrow?” The bank starts elsewhere. It asks, “How much of your monthly income is already committed?”

That gap matters. I've seen buyers with high earnings assume the file would be simple, only to discover that a car loan, two credit cards, school-fee financing, and an existing mortgage abroad push the debt burden too far in the bank's model. I've also seen modest-looking files pass cleanly because the income was stable, the obligations were limited, and the presentation was disciplined.

French banks are rarely impressed by income in isolation. They want to know what remains after recurring obligations are counted. For non-residents, that analysis becomes stricter because the bank may also review how reliable the foreign income is, how it converts into euros, and whether the legal structure of the purchase adds complexity.

A strong French mortgage file isn't built on headline income. It's built on usable income.

Many buyers lose time when they compare themselves to local borrowers, use a generic online calculator, and assume the result applies to them. It usually doesn't. A London employee paid in GBP, a Dubai consultant billing through a company, and a U.S. investor buying via an SCI may all have similar earnings on paper and very different outcomes in practice.

The good news is that DTI isn't mysterious once you break it down properly. It's a practical underwriting tool. Used well, it helps you decide whether to reduce debt first, wait for stronger documentation, change the structure, or move forward now with confidence.

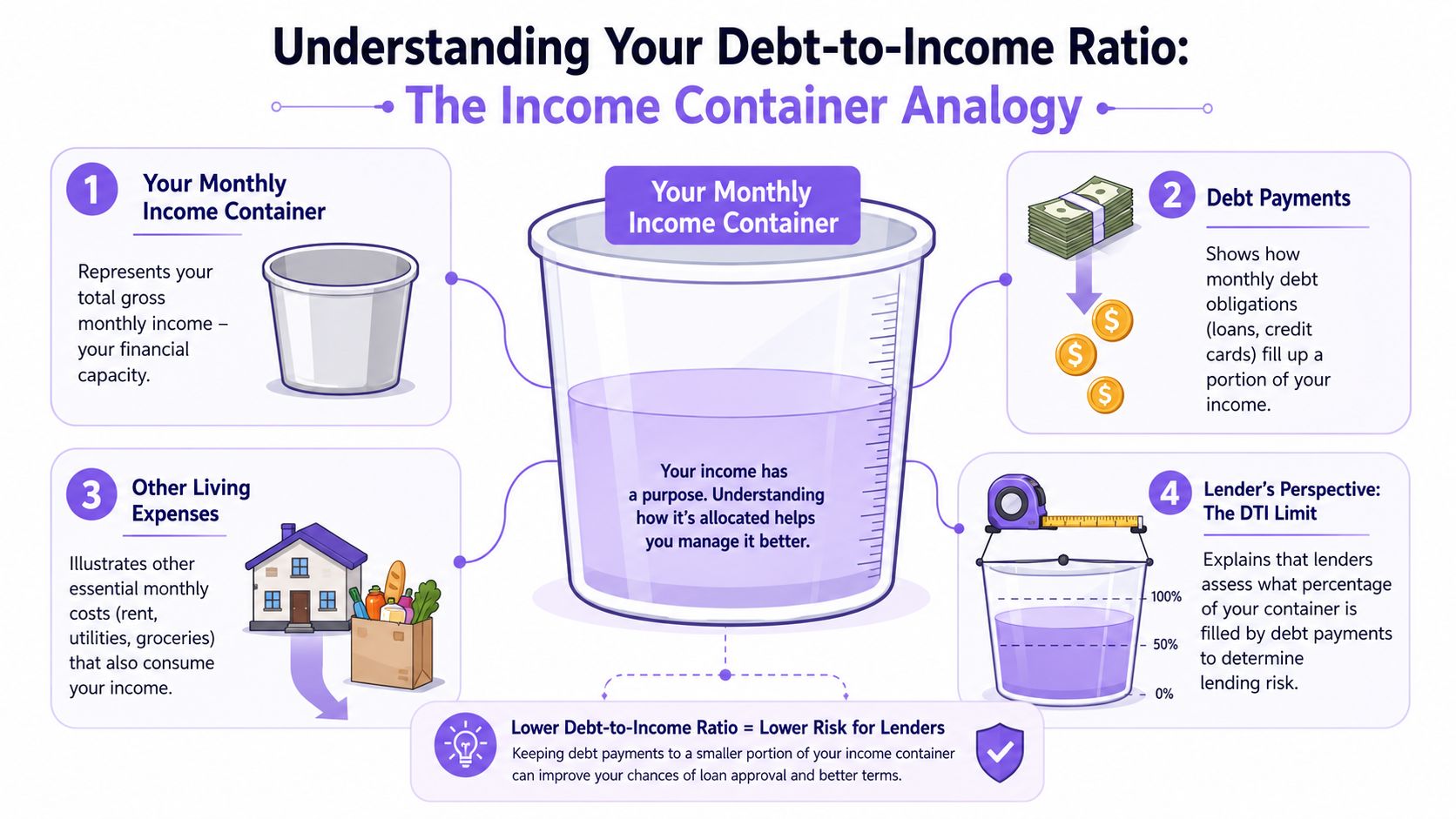

What Exactly Is the Debt-to-Income Ratio

Debt-to-income ratio, or DTI, measures how much of your gross monthly income is already committed to recurring debt payments. The standard formula is monthly debt payments divided by gross monthly income, multiplied by 100, as explained by Navy Federal's guide to debt-to-income ratio.

For a French mortgage, that percentage is one of the first filters a bank applies. It helps the underwriter judge whether the new loan fits inside your existing monthly commitments, not just whether your income looks high on paper.

This matters even more for expats and non-residents. A borrower paid in euros with a standard salaried contract is easier for a French bank to assess than a borrower paid in dollars, dirhams, or pounds, or one earning through dividends, a foreign company, or an SCI structure. The ratio is still the same. The bank may reduce the income it is willing to count before applying it.

Front-end and back-end ratios

Lenders often separate DTI into two views:

Front-end ratio looks only at housing costs

Back-end ratio looks at all recurring monthly debts

In French mortgage underwriting, the back-end view usually carries more weight because it reflects your full monthly burden. A file can look comfortable on property costs alone and still be refused if other obligations already absorb too much income.

For non-residents buying in France, that distinction is practical. Existing mortgages abroad, personal loans, credit card minimums, maintenance payments, and certain business-related commitments can all affect the decision. Buyers who want a quick sense check before submitting a file can use this outil de calcul de prêt, but the bank's final assessment will still depend on what it accepts as usable income.

Why this ratio matters so much in France

French banks do not use DTI as a rough budgeting tip. They use it as a credit risk threshold.

In many standard owner-occupier cases, banks in France work around a debt burden limit of roughly 35 percent including insurance, in line with HCSF guidance. In practice, some profiles can be treated more flexibly, but non-resident files are rarely where banks become generous. If income is foreign, variable, or exposed to exchange-rate risk, the underwriter may apply a haircut to that income and the effective ratio rises fast.

That is where generic DTI advice becomes misleading. A U.S. guide may tell you one ratio is acceptable, but a French lender can reach a different result because it weighs foreign income differently, excludes part of bonus income, or takes a cautious view of rental income held through an SCI.

Practical rule: French banks assess repayment capacity based on income they trust, in a form they can document, after recurring commitments are fully counted.

That is the definition borrowers need. DTI is not just a percentage. For an expat buying in France, it is the percentage after currency risk, legal structure, and document quality have been factored into the bank's view of your file.

How Lenders Calculate Your DTI Ratio

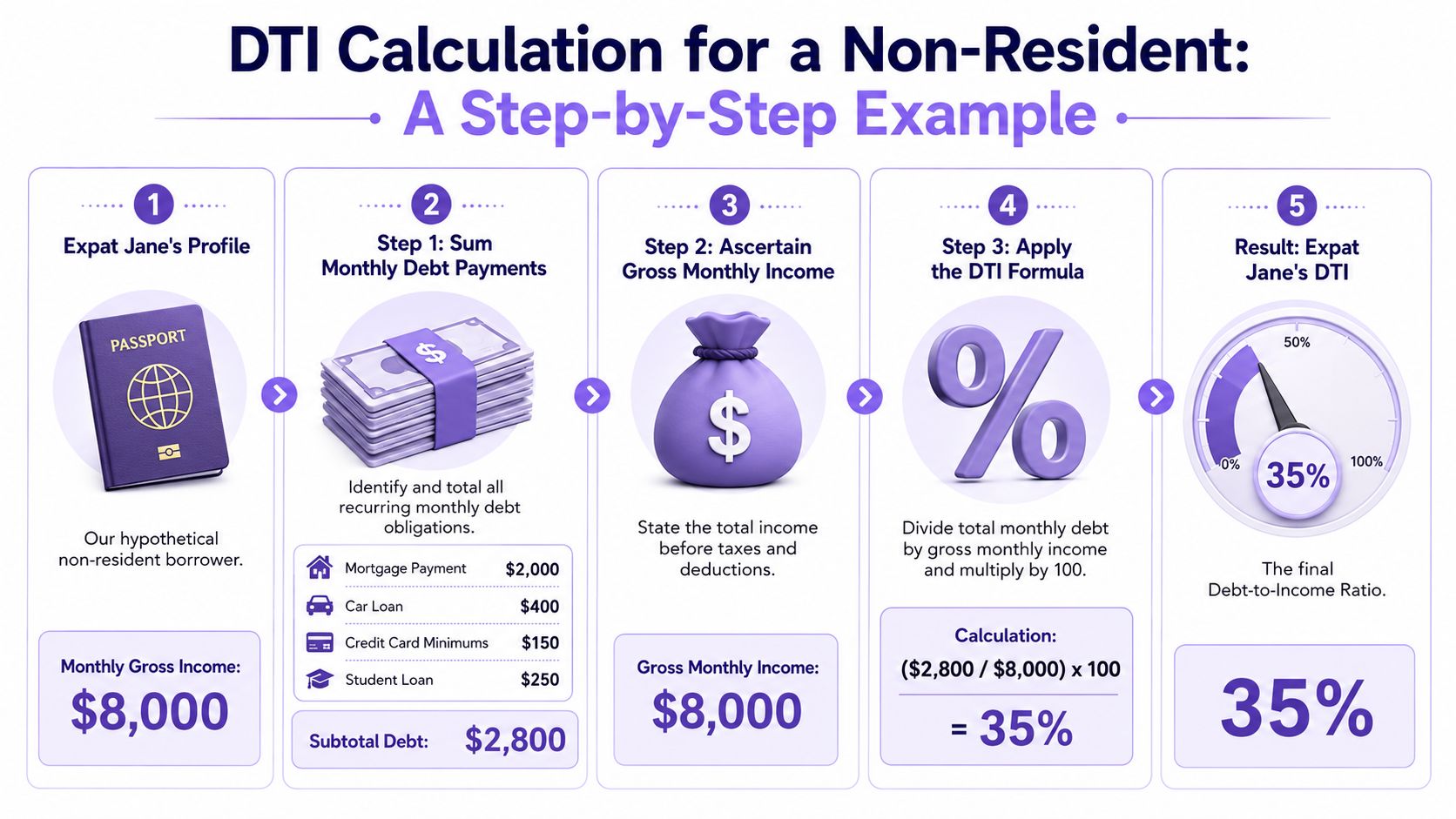

The formula itself is straightforward. The issue is how the bank builds each side of the equation. For a non-resident file, that's where most surprises happen.

The Consumer Financial Protection Bureau defines DTI as all monthly debt payments divided by gross monthly income, and notes that in U.S. mortgage underwriting Fannie Mae uses 36% as the standard manual benchmark, 45% as a conditional ceiling with compensating factors, and 50% as the maximum for certain DU findings. It also notes that a strong application combines an acceptable debt burden with stable income, as set out by the Consumer Financial Protection Bureau's DTI explanation.

The basic calculation

Start with two figures:

Total monthly debt payments

Gross monthly income

Then divide the first by the second and multiply by 100.

The infographic above shows a simple example: monthly income of $8,000, total monthly debt payments of $2,800, which produces a 35% DTI. That kind of arithmetic is easy. What isn't easy is deciding what the bank will accept as income, especially if it's foreign, variable, or company-based.

How French banks read a non-resident file

A French bank usually doesn't stop at the salary line on your payslip. It wants to know whether that income is stable, understandable, and transferable into its own risk framework.

For salaried applicants paid abroad, the bank commonly asks questions like these:

Currency exposure

If your income is in USD, GBP, AED, CHF, or another currency, the bank may not treat it as identical to euro income. The issue isn't only exchange conversion. It's volatility and how underwriting policy handles that risk.Contract structure

A permanent local contract and an expat package may be read differently. The bank looks for continuity, employer quality, and evidence that the income stream is sustainable.Variable pay

Bonus, commission, RSUs, or profit-sharing can help a file, but only if they're well documented and shown as recurring rather than exceptional.Document consistency

If your tax returns, bank statements, employment letter, and payslips don't align cleanly, the underwriter often becomes conservative.

Many non-resident borrowers don't fail because they earn too little. They fail because the bank can't stabilize the income confidently enough.

Why your own estimate may be wrong

A borrower often calculates DTI using their full earnings and a rough list of debts. The bank's version can look less generous.

It may convert your income into euros, review whether all of it should be retained, and separate fixed salary from variable or less predictable components. On the debt side, it won't ignore obligations just because they sit in another country. Existing mortgages, personal loans, and minimum card payments still matter if they are recurring liabilities.

That's why a pre-application review is so useful. If you want to test scenarios before going to market, an outil de calcul de prêt can help you model the effect of income, debt, and project size before a bank gives its own reading.

What works and what doesn't

What works is presenting a file that is easy to underwrite. Clean statements, clear debt schedules, stable proof of income, and realistic borrowing assumptions help. What doesn't work is assuming the lender will “average things out” in your favor.

For non-residents, the strongest files are rarely the most complicated. They're the most legible.

What Counts as Debt and Income for a French Mortgage

Most mistakes happen here. Buyers either include too little, because they assume some foreign debts won't matter, or they include too much, because they confuse daily spending with underwritten debt.

According to Cornell Law School's overview of debt-to-income ratio, lenders typically include minimum credit-card payments, monthly loan installments, and housing costs, while excluding many living expenses. The same source also notes that recurring obligations such as student loans, auto loans, or child support can change a file materially because lower DTI generally improves approval probability by reducing perceived repayment risk.

The debt side

Here is the practical test. If it's a recurring monthly obligation that a lender can verify and that reduces your ability to service a new mortgage, it usually counts.

Category | What's Included | Expert Note for Expats |

|---|---|---|

Existing property debt | Mortgage payments on your home or investment properties | Foreign mortgages are still part of the picture if they remain in your name |

Consumer loans | Car loans, personal loans, student loans, installment debt | Even small monthly amounts can matter when the file is already tight |

Revolving debt | Minimum credit-card payments | Banks usually focus on the minimum required payment, not what you choose to repay voluntarily |

Family obligations | Child support, alimony, similar recurring commitments | These are underwriting obligations, not optional spending |

Housing costs on the new purchase | The future mortgage-related monthly charge assessed in the file | This is the amount that completes the lender's affordability test |

Daily living costs | Groceries, utilities, transport, subscriptions | Usually not counted in DTI, though they still matter to your real-life budget |

The income side

Income is more nuanced than debt because banks don't just ask whether you receive it. They ask whether they can rely on it.

For salaried applicants, the easiest income to use is generally fixed employment income supported by consistent documentation. Variable components can strengthen the file when they're regular and well evidenced. Rental income, investment income, and company distributions may also help, but only when the lender can understand the source, continuity, and any deductions that should apply.

A useful parallel here is how gross income impacts budgeting. That framework helps borrowers distinguish between income that looks strong in daily life and income that underwriters can use in a mortgage analysis.

Common points of confusion

Borrowers often get tripped up by a few recurring issues:

Using net income instead of gross income

DTI is generally built from gross monthly income in standard underwriting logic.Ignoring minimum card payments

Even if you clear the balance aggressively, the lender often looks at the mandatory payment.Assuming foreign rental or company income will be read at face value

It may be usable, but it usually needs stronger documentation and clearer presentation.Mixing lifestyle cost with underwritten debt

School fees, travel, or private club memberships may affect your personal comfort but don't always enter the formal DTI calculation.

The cleaner your categorization, the more accurate your borrowing assessment will be before the application even starts.

Special DTI Rules for Unique Non-Resident Profiles

Generic DTI advice breaks down quickly once the borrower isn't a standard employee living and earning in one country. The better question isn't “What's a good ratio?” It's “How will the lender interpret my profile?” That distinction is exactly what Alltru Credit Union's discussion of nuanced borrower profiles points to, especially for expat employees, founders, and SCI or co-borrowing structures.

Salaried expats

A salaried expat usually has the most straightforward route, but only if the contract and payslips are easy for the bank to read. A permanent employment arrangement with a recognized employer is easier to underwrite than a contract with irregular allowances, mobility clauses, or a compensation package made up of many moving parts.

The main issue isn't just salary level. It's whether the underwriter sees the income as durable and easy to normalize into the file. Housing allowances, school allowances, relocation benefits, and performance elements may or may not strengthen affordability depending on how they appear in the documents.

Entrepreneurs and freelancers

This profile is where many banks become cautious. A company owner may earn well and still struggle to prove stable personal income in a format the lender accepts. Dividends, director remuneration, retained profits, and cross-border corporate structures require interpretation, not just translation.

That's why founders and freelancers need a different preparation process. Clean accounts, tax consistency, and a clear story about how income flows from business to borrower matter more than polished presentation. For a deeper look at this category, financing for non-resident entrepreneurs is worth reviewing before you approach lenders.

The more complex the income, the more the bank values consistency over ambition.

Real estate investors

Investors often assume prior property ownership will reassure lenders automatically. Sometimes it does. Sometimes it complicates the file because every existing mortgage, every rental stream, and every vacancy risk has to be interpreted.

A borrower with several assets can still be financeable in France, but the file must show control. The lender wants to understand whether the existing portfolio supports the new acquisition or strains the monthly picture. Strong asset ownership helps only when the debt side remains coherent.

SCI structures and co-borrowing

SCI purchases create a different layer of analysis. The bank won't just ask whether the property is attractive. It will examine who the shareholders are, how repayment will be supported, and whether the co-borrowers' income and liabilities are aligned.

In cross-border SCI files, the practical challenge is coordination. Different tax residences, different currencies, and different personal debt positions can make the same purchase look simple on paper and complex in underwriting. A good structure can help. A vague one usually delays approval.

How to Improve Your DTI for a Stronger Application

A non-resident file can look strong at first glance and still fail on affordability. I see it often with applicants paid in dollars, pounds, dirhams, or Swiss francs. The income is good, but the bank applies a haircut to foreign currency earnings, keeps all existing monthly commitments, and the ratio ends up tighter than expected.

The practical fix is to change what the bank counts. In France, that usually means lowering monthly debt already visible on your statements or presenting income in a form the lender will retain with confidence. Small lifestyle adjustments rarely change the underwriting result.

Five actions that usually work

Clear revolving debt before the file goes to the bank

Credit cards, overdraft facilities, and personal lines of credit are common problems in expat files. Even when the outstanding balance feels manageable, the monthly commitment can weigh heavily in the French calculation. If the balance is repaid, the proof needs to be visible in statements and supporting documents before submission.Restructure debt only if the monthly payment really falls

Consolidation helps when it reduces the recurring charge the bank must include. If it only repackages debt without improving the monthly position, it does little for mortgage capacity. I also check whether an early repayment or refinance creates new fees that weaken your liquidity just before completion.Apply when your income is at its most bankable

Timing matters. A recent raise may not be fully retained yet. Variable compensation may need a longer track record. For self-employed borrowers and company directors, filed accounts often carry more weight than internal management numbers, even if those management numbers are more current.Pause new borrowing until the mortgage is agreed

A car loan taken three months before application can reduce borrowing power more than many buyers expect. The same applies to buy-now-pay-later instalments, margin loans, and personal loans used for renovations or furnishing. French banks review the full monthly picture, not just the future mortgage payment.Use more equity where it solves the right problem

A larger deposit can reduce the loan amount and improve the overall case, especially for non-residents who already face stricter policy filters. It does not always cure a stretched DTI on its own, but it can help bring the payment back within the bank's threshold and reassure the lender on risk.

What usually does not change the outcome

Some ideas sound sensible but have little impact once the file reaches underwriting.

Reducing everyday spending for a short period does not help if your fixed monthly liabilities stay the same.

Saying a debt will disappear soon has little value unless it is already repaid and documented.

Sending partial evidence of bonus, dividend, or freelance income often leads the bank to exclude part of it.

Keeping debt in another country because it feels separate does not work if it still appears as a personal obligation.

Using an SCI without a clear repayment logic can complicate the file rather than improve it, especially if the shareholders have uneven incomes or debts in different jurisdictions.

For entrepreneurs with U.S. activity, separate planning around obtaining US business credit can help keep company borrowing distinct from personal mortgage affordability. The benefit disappears if business debt is supported by a personal guarantee that creates a monthly burden the French bank decides to count.

One practical tool

For non-residents who want to structure the file before approaching banks, Invexa acts as a specialist mortgage brokerage for expatriate and non-resident purchases in France. That review can be useful when the issue is not only the ratio itself, but also how a lender will treat foreign currency income, existing property debt, co-borrowers, or an SCI purchase.

Master Your DTI and Secure Your French Mortgage

DTI is the number that brings discipline to a French mortgage application. It tells the lender whether your income can support the new debt once your existing obligations are fully counted. For expats and non-residents, that test becomes more technical because foreign income, multiple jurisdictions, variable earnings, and SCI structures all affect how the file is read.

That's why understanding debt to income ratio is so valuable before you start submitting documents. It helps you separate what looks strong from what is financeable. It also shows where to act. Sometimes the answer is to repay a revolving balance. Sometimes it's to wait for cleaner accounts. Sometimes it's to change the borrower structure before going to market.

A good French mortgage application isn't only about earning more. It's about presenting a profile the bank can underwrite with confidence. When that's done properly, DTI becomes a manageable metric rather than a frustrating surprise.

If your project involves foreign salary, self-employed income, existing property debt, or an SCI purchase, getting the ratio right at the start can save a great deal of time and avoid avoidable refusals.

If you want a clear view of how a French bank is likely to assess your file, Invexa offers a free and confidential consultation for expatriates and non-residents buying property in France. A focused review can show how your debt, income, currency exposure, and purchase structure fit together before you commit to the next step.