How to Calculate Mortgage Affordability in France

Learn how to calculate mortgage affordability for property in France (non-resident). Guide covers formulas, foreign income, and tips to boost capacity.

published

Outrank AI

how to calculate mortgage affordability, mortgage for expats, buying property in france, non-resident mortgage, french mortgage calculator

4c5eef39-b6ab-4524-9f5f-f290c806355c

You're probably doing what most non-resident buyers do at the start. You have a rough income figure in your head, a target property in France, and a mortgage amount that feels plausible. Then you open a generic calculator and realise it doesn't ask the questions your bank will ask.

That gap matters. A French bank doesn't look at affordability the same way a broad consumer calculator does, especially if your salary is paid abroad, your income comes in a foreign currency, or your tax situation spans more than one country. If you want to know how to calculate mortgage affordability for a French purchase, you need to think like the lender reviewing your file.

For expats, that means focusing on three things from the beginning: how the bank defines usable income, which debts it counts, and how it treats uncertainty such as variable earnings, bonuses, and exchange-rate risk. Once you understand that framework, the numbers become far less mysterious.

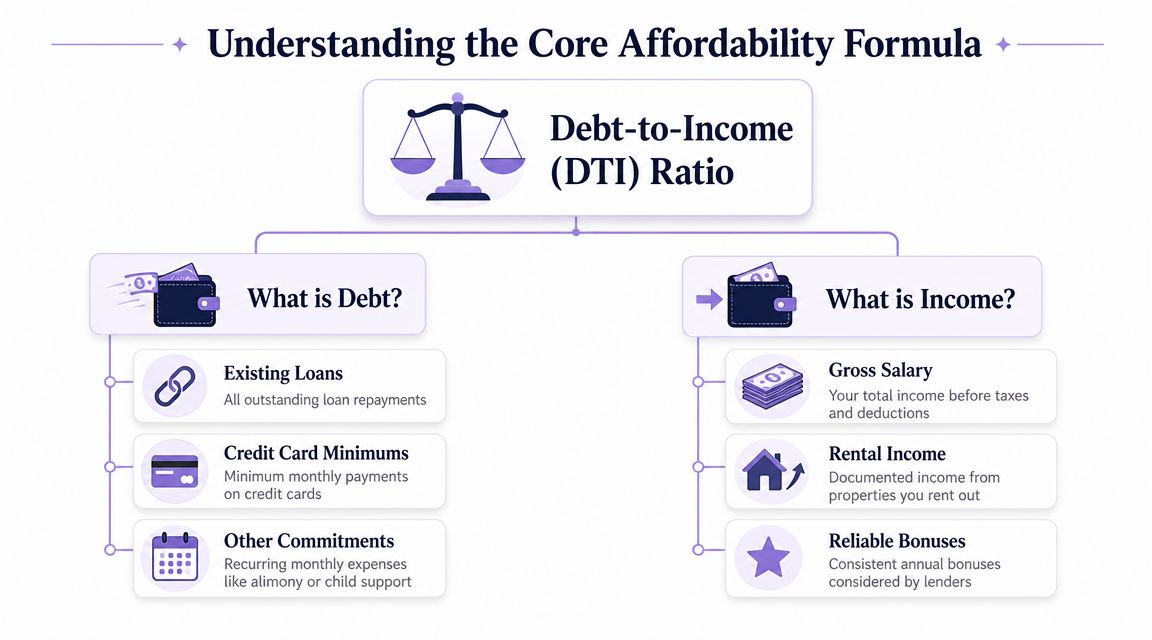

Understanding the Core Affordability Formula

A buyer in Dubai, London, or New York can look affordable on paper and still fail a French bank's first review. I see this regularly with expats whose income is strong, but paid in dollars, dirhams, pounds, or a mix of salary, bonus, and self-employed earnings. The bank is not only asking how much you earn. It is asking how much of that income it is willing to count, in euros, after applying its own caution.

That is the core formula:

Affordability formula:

Counted monthly income ÷ total monthly debt obligations = debt capacity available for housing

Or, viewed from the lender side:

Total monthly debt obligations ÷ counted gross monthly income = affordability ratio

International buyers often start with broad DTI rules from their home market. That can be useful as a rough sense check, but it misses what matters in France for non-residents: the bank may haircut foreign income, convert it conservatively, and include debts you would not expect a generic calculator to pick up.

What counts as debt

French lenders do not isolate the future mortgage payment. They review your full recurring monthly commitments because each one reduces the room available for a new loan.

Typical items include:

Existing loan repayments, such as car finance, personal loans, student loans, and mortgages on other properties

Credit card obligations, especially where statements show revolving balances or consistent minimum payments

Maintenance or support payments, where legally required and documented

Other recurring commitments, if they are contractual, visible on statements, and likely to continue

The mistake I see most often from US-based and Middle East-based buyers is that they model only the new French mortgage and ignore debts already running in another country. A bank usually will not. If there is a monthly obligation on your statements or credit file, assume it needs to be disclosed and tested.

What counts as income

Gross income is the starting point, but for expats the more important question is counted income. Those are not always the same number.

Lenders usually begin with:

Base salary

Documented rental income

Recurring professional income

Bonus or commission income, if the history is stable and the bank accepts it

Dividend or self-employed income, if supported by tax returns, company accounts, or accountant documentation

For non-residents, documentation quality matters almost as much as the amount. If your salary lands in one country, your bonuses in another, and your tax returns are filed under a different system, the bank will want a clean trail from contract to payslip to bank statement to tax filing. For buyers sorting multiple accounts and foreign inflows, PDF AI's finance analyzer can help organise statement patterns before you compare them with lender criteria.

A practical first-pass formula

Use this before speaking to a bank:

Maximum total monthly debt allowed - existing monthly debt = room for the new housing payment

For an expat buyer, the challenge is that both parts of that formula can move. Existing debt may sit in another jurisdiction. Income may be converted from a foreign currency and reduced by the lender before the ratio is even calculated.

A better first estimate is to start with the inputs French banks care about, using a French mortgage calculator, then adjust your file for foreign income quality, debt visibility, and currency risk.

A simple example

Take a borrower earning the equivalent of €10,000 gross per month from overseas employment, with €1,200 of existing monthly loan payments.

A generic affordability model might suggest that income alone supports a fairly high payment. A French lender will usually ask a narrower question: after all existing debts are counted, how much room is left for the new mortgage once accepted income has been converted and adjusted?

Using the basic structure above:

Counted monthly income cap for debt - existing monthly debt = available mortgage capacity

If the bank accepts the full income, the buyer looks stronger. If it discounts part of the bonus, applies a buffer to foreign currency income, or excludes some variable earnings, borrowing power falls quickly. That is why expat affordability in France is not just an income question. It is a counted-income question.

How French Banks Calculate Your Taux d'Endettement

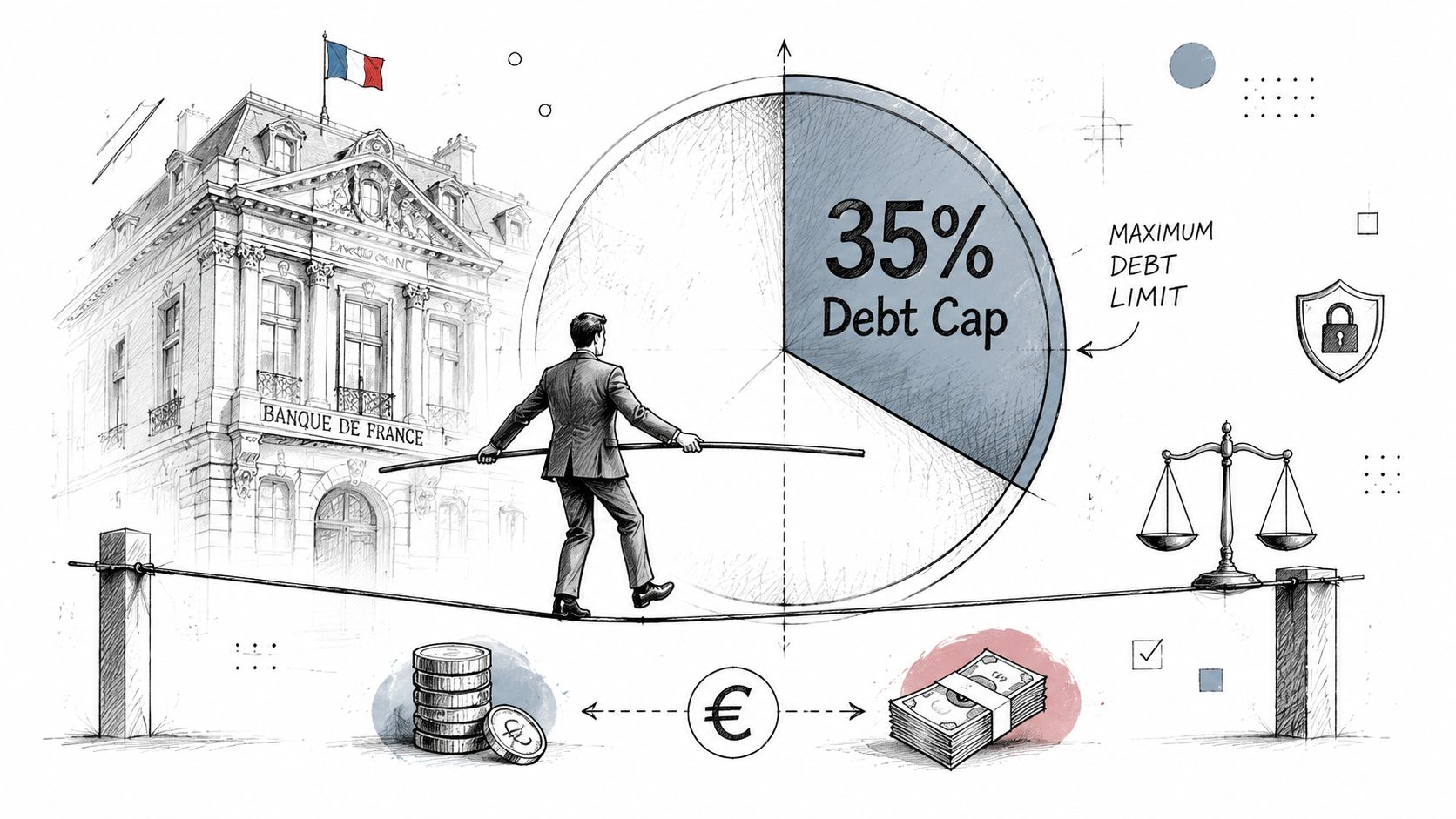

French banks use a stricter affordability lens than many international borrowers expect. The core metric is taux d'endettement, the debt ratio used to judge whether your total monthly obligations stay within an acceptable share of income.

For benchmarking, the National Association of REALTORS® methodology uses a 25% qualifying ratio for principal and interest when building its housing affordability index. That contrasts with the stricter 35% total debt ratio used for actual loan underwriting in France (NAR affordability methodology).

That single difference changes how you should build your budget. In France, the question isn't “what mortgage could I maybe qualify for under a flexible range?” It's “does my full monthly debt load fit inside a tighter cap once the bank has adjusted my income?”

What French banks usually include

French underwriting tends to be more thorough than the assumptions many expats bring from the U.S., UK, Singapore, Dubai, or Hong Kong.

A bank will usually assess:

Your counted monthly income, not necessarily your full headline income

Your existing monthly loan payments

The projected new mortgage payment

Other recurring obligations that affect your real monthly capacity

That's why buyers with strong salaries still get surprised. The salary itself may look high, but the bank may only accept part of it, especially if the file includes bonuses, dividends, freelance income, or currency exposure.

The practical formula

The working logic is straightforward:

French affordability rule of thumb:

Total monthly debt obligations ÷ monthly income accepted by the bank = taux d'endettement

The result generally needs to stay within the French lending cap used in underwriting.

Many online calculators fail for non-residents. They let you enter a gross income number, but they don't ask how much of that income a French lender will keep after reviewing contracts, payslips, tax returns, and exchange-rate risk.

A euro-based illustration

Suppose a borrower has monthly income in euros that the bank fully accepts. The bank first calculates the maximum total monthly debt load allowed under the French cap. Then it subtracts any existing debt payments. What remains is the maximum room for the new housing payment.

That sequence matters:

Start with the bank-accepted monthly income

Apply the French debt-ratio cap

Subtract all existing recurring monthly debts

The remainder is the maximum mortgage-related monthly payment

Here's the practical takeaway. A borrower with no other debt and a clean salaried profile may have room for a much stronger offer than a borrower with the same headline income but multiple monthly obligations abroad. The issue isn't only income size. It's the composition of the file.

For readers who want a broader primer on qualifying for a mortgage based on DTI, that framework is useful. Just remember that French banks apply it with a different level of rigidity, particularly for non-residents.

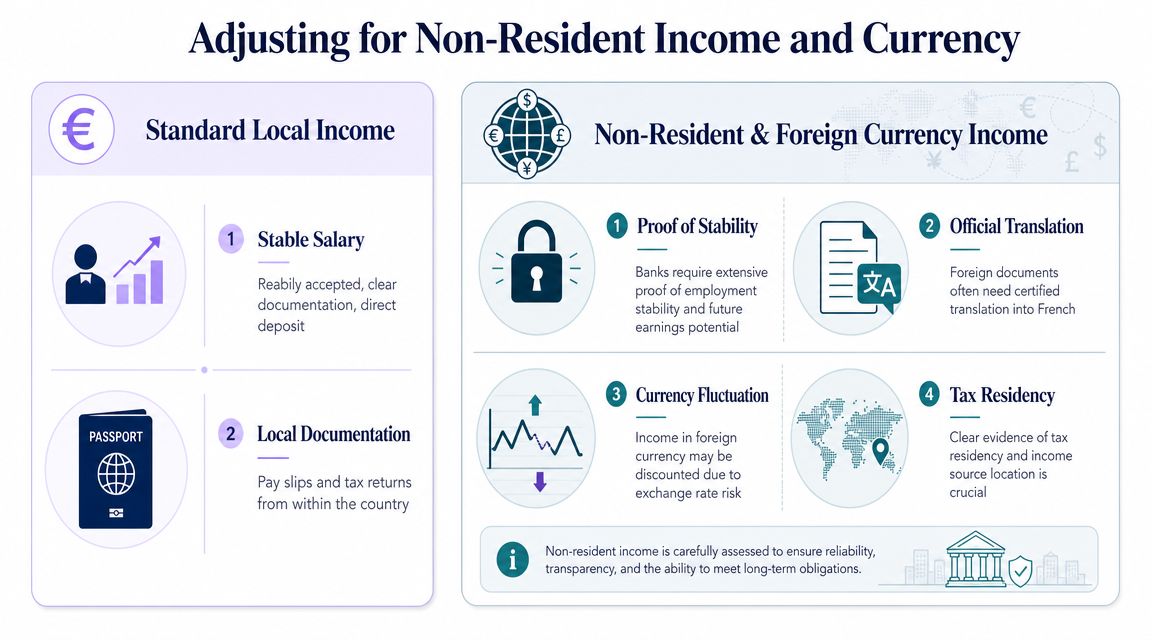

Adjusting for Non-Resident Income and Currency

Expat files move beyond mechanical assessment and become judgment-based. A French bank rarely treats foreign income at face value without asking deeper questions. It wants to know whether the income is stable, whether it is easy to document, whether the borrower's tax position is coherent, and whether exchange-rate movements could weaken repayment capacity.

Chase's affordability guidance captures the core issue well: many tools assume stable monthly gross income, but for expatriates, entrepreneurs, and investors, the issue is the bankability and weighting of income streams, not just the formula (Chase affordability guidance).

What banks are really testing

For a French lender, foreign income introduces several layers of risk at once.

Employment risk. Is the job stable, long-term, and easy to verify?

Currency risk. Could exchange-rate moves reduce the euro equivalent of your income?

Documentation risk. Are payslips, tax returns, company accounts, and contracts clear enough for a French credit committee?

Tax coherence. Does your declared income line up with your residency, corporate structure, and source of funds?

This is why two borrowers with the same nominal annual pay can receive very different affordability outcomes.

Why standard calculators miss the point

Generic calculators usually assume one monthly income figure and one debt figure. That's fine for a domestic salaried borrower paid in local currency. It breaks down quickly for an expat profile.

Common blind spots include:

Foreign currency salaries that may be converted conservatively

Variable compensation such as bonus, commission, RSUs, or freelance income

Self-employed structures where the bank reviews company accounts, not just drawings

Cross-border tax situations where usable income must be reconciled across jurisdictions

If you're dealing with that kind of profile, a specialised resource like the guide Invexa du crédit immobilier expatrié is more relevant than a simple domestic affordability tool.

How weighting works in practice

French banks often apply internal weighting rules rather than accepting every income component equally. Those rules vary by bank, file quality, currency, and profession, so there is no universal public grid you can plug into. But the direction of travel is consistent.

A lender may view income in broad categories like these:

Income type | Typical bank view |

|---|---|

Local salaried income in euros | Usually the easiest to accept if documentation is clean |

Salaried income in major foreign currency | Often acceptable, but the bank may apply a conservative conversion or buffer |

Bonus or commission income | Often considered only if it is regular and well documented over time |

Self-employed income | Usually reviewed with more scrutiny and more supporting documents |

Dividend-heavy income | Often treated more cautiously than fixed salary |

Rental income abroad | May be considered, but often after review of evidence and ongoing charges |

The important point isn't the exact weighting. It's that weighting exists. A borrower earning abroad should never assume that the full top-line income will flow directly into the French affordability calculation.

A practical formula for expats

For non-residents, the useful affordability formula looks more like this:

Bank-accepted income = foreign gross income converted to euros, then adjusted for how the bank weights each income stream

After that, the bank applies the French debt-ratio rule to the accepted income, not to your headline earnings.

That's the formula most standard articles miss. They explain affordability as if the only question were monthly income multiplied by a fixed ratio. In real non-resident lending, the first fight is getting the right income number onto the page.

What strengthens a foreign-income file

A bank gets more comfortable when the story is simple and evidenced. In practice, that means:

Stable employment under a clear contract helps more than a fast-growing but thinly documented startup story.

Consistent inflows into the same account make income easier to verify.

Clean tax returns reduce questions about what income is recurring and usable.

Certified translations can remove friction if key documents aren't in French.

A coherent explanation of currency exposure helps if your expenses and assets are partly matched to the income currency.

Buyers often focus on the property too early. For expats, the bank starts with the income architecture. Get that right first.

A Complete Worked Example for an Expat Buyer

A typical expat file looks straightforward until a French bank starts recalculating it. A French citizen living in Singapore earns a strong salary in SGD, receives an annual bonus, and wants to buy an apartment in Paris as a non-resident. An online calculator may suggest a comfortable budget. The French lender will rebuild the case from scratch, in euros, with haircuts on variable income and full visibility on existing debts.

Here is a worked example using realistic bank logic.

Assume the borrower has:

Base salary: S$12,000 per month

Average bonus: S$3,000 per month, based on the last 3 years

Car loan: €400 per month

Personal loan: €150 per month

Target purchase: Paris apartment for personal use during stays in France

Loan term considered: 20 years

A bank first converts the income into euros using its own internal rate, not the most flattering live FX quote the borrower sees on a currency app. For this example, assume the bank converts:

S$12,000 base salary = €8,200

S$3,000 bonus = €2,050

That gives a headline monthly income of €10,250.

Now the underwriting starts. French banks usually accept the fixed salary more readily than bonus income. If the bonus is consistent and well documented, a lender may accept only part of it. In this example, the bank takes:

100% of base salary = €8,200

50% of bonus = €1,025

So the bank-accepted income = €9,225 per month.

That number matters more than the borrower's gross income.

Next, the bank applies the French debt ratio, the taux d'endettement, to the accepted income. Using a 35% ceiling for total monthly debt:

Maximum total debt load = €9,225 × 35% = €3,228.75

Then it subtracts existing monthly commitments:

Available room for the new French mortgage = €3,228.75 - €400 - €150 = €2,678.75

Rounded, this borrower can support a maximum housing payment of about €2,679 per month, assuming the rest of the file is clean.

For an expat, that payment is not just principal and interest in the abstract. The bank will also look at the full cost structure around the property and at the stability of the foreign income behind it. If the income arrives in SGD but the mortgage is in euros, the lender is also judging currency risk. A borrower paid in a volatile currency, or one with uneven bonus history, can see the accepted income reduced further.

Now turn that monthly capacity into a rough loan amount.

At an example rate of 4.00% over 20 years, a monthly payment of €2,679 supports a loan of roughly €440,000 to €445,000, before adjusting for other property-related costs the bank may include in its internal affordability view. If the borrower wants to stay conservative, I would usually work from the lower end of that range.

So the file looks like this:

Bank-accepted income: €9,225

Maximum total debt at 35%: €3,228.75

Existing debts: €550

Maximum new mortgage payment: €2,678.75

Estimated borrowing capacity over 20 years at 4.00%: about €440,000

Many non-resident buyers often make a mistake here. They start from €10,250 of converted income and assume the bank will lend against all of it. In practice, the actual starting point is €9,225, and sometimes less if the lender is cautious on bonus income, foreign tax complexity, or exchange-rate exposure.

A second version of the same file shows how sensitive the result can be. If the bank accepts only 30% of the bonus instead of 50%, accepted income falls to €8,815. At a 35% debt ratio, maximum total debt becomes €3,085.25. After the same €550 of existing loans, the available mortgage payment falls to €2,535.25. That can reduce borrowing capacity by tens of thousands of euros.

This is why expat affordability work has to be done with the bank's weighting rules, not generic debt-to-income assumptions imported from the U.S. market. The practical question is not “What do you earn?” It is “What will this French bank accept, after currency conversion, income weighting, and debt capture?”

At Invexa, this is the calculation we build first for clients exploring non-resident property financing in France. It gives a usable range before you waste time targeting properties that a French lender is unlikely to support.

Proven Strategies to Increase Your Borrowing Capacity

Affordability isn't fixed. In many expat files, the first version of the numbers is only a draft. A borrower can often improve the result by changing what the bank sees as risk.

The most effective approach is to work backward from the monthly payment you want to keep comfortable. The CFPB recommends starting with a realistic total monthly home payment, then subtracting estimated property taxes and homeowners insurance to find the amount available for principal and interest. It also warns that many borrowers overestimate affordability by ignoring these recurring costs, which can materially reduce the loan size they can support (CFPB homebuying guidance).

Changes that usually help

Some levers are much more powerful than others because they directly address lender concerns.

Reduce existing debt. A car loan or personal loan doesn't just cost cash each month. It occupies debt-ratio space that could otherwise support the French mortgage.

Increase the down payment. A larger contribution lowers the amount financed and usually makes the file look stronger.

Simplify the income story. If you can present stable salary cleanly and avoid relying on hard-to-defend variable income, the bank's comfort level often improves.

Clean up documentation. Missing pages, inconsistent tax documents, and unexplained transfers create friction that can lead to a more conservative reading of the file.

Use a co-borrower carefully. Combined income can help, but only if the second borrower's debts and documentation don't create new problems.

Trade-offs that matter in France

Not every “improvement” is an improvement.

A longer term can reduce the monthly payment, which may help the debt ratio. But it doesn't cure weak documentation or unstable income. Similarly, a high headline income doesn't help much if the lender discounts a large part of it.

I often tell expat buyers to focus on the variables banks can trust:

Predictable salary

Visible savings behaviour

Low recurring debt

Clear source of funds

Tax consistency across countries

Those factors don't just make approval more likely. They also give the bank room to be less defensive when it reviews the file.

Structuring the project properly

Non-residents sometimes also need to think about ownership structure, not just affordability. Depending on the project, a direct personal purchase may work better, or an entity structure may be more appropriate. The right choice depends on tax, succession, income type, and the bank's preferences.

For buyers comparing options around non-resident property financing in France, it helps to model the financing structure before making an offer. That's one of the few moments where getting technical early saves time.

A stronger mortgage application is usually not the one with the most documents. It's the one where the numbers, tax profile, and source of income all tell the same story.

If you want the bank to stretch, remove uncertainty first. Pay down debts that can be cleared. Present translated and consistent paperwork. Keep large unexplained account movements out of the file where possible. And don't anchor your purchase budget to the most generous calculator you can find. Anchor it to the number a French underwriter is likely to accept.

If you want a realistic affordability assessment for a French purchase as an expat or non-resident, Invexa works specifically on cross-border mortgage files. The practical value is straightforward: your income, debts, currency exposure, and documentation are reviewed through the lens French banks use, so you can target the right property budget before you commit.