Understanding Power of Attorney for France Property Deals

Your guide to understanding power of attorney for French property deals. Learn how to draft, notarize, and use a 'procuration' from abroad as an expat.

published

Outrank AI

understanding power of attorney, french power of attorney, procuration france, buying property in france, expat mortgage france

356794e4-f9de-4e89-bcec-0ed8c2cec092

You're ready to buy in France. The offer is accepted, your financing is moving, and the notary has started preparing the closing file. Then the practical problem appears. You're not in France, you can't travel at short notice, and the signing date for the acte de vente won't wait for your flight schedule.

That's the moment when understanding power of attorney stops being a legal theory and becomes a closing tool. For non-resident buyers, a French procuration is often what keeps the purchase on track when distance, work commitments, or family logistics make in-person signing unrealistic.

Most guides explain the definition. Very few explain what matters in a live transaction: who drafts it, what format the French notary will accept, whether apostille or legalization is needed, when remote notarisation works, and what can delay acceptance. Those are the points that decide whether your purchase closes smoothly or turns into a scramble.

Your Key to Buying French Property from Abroad

A common situation looks like this. The notary confirms the signing date. The bank file is almost complete. The seller wants certainty. But you're in London, Dubai, New York, Singapore, or Toronto, and getting to France in time is either expensive, inconvenient, or impossible.

In that setting, a power of attorney, called a procuration in France, lets a trusted person sign the purchase deed on your behalf. Used properly, it is one of the cleanest ways to complete a French property purchase remotely.

The stress point for most buyers isn't the concept. It's execution. As the National Council on Aging explains in its POA guidance, the primary issue is often not “what is a POA?” but what document format will be accepted, and how to complete it in time. Without a valid, properly authenticated POA, families can face significant delay or even court intervention.

Why this matters in a real purchase

French property transactions run on documents, dates, and formalities. If your POA arrives late, is drafted too vaguely, or doesn't meet the notary's standards, the notary may refuse to use it. That can affect the deed signing, mortgage release, and handover of funds.

Practical rule: In a French purchase, a POA only helps if the notary accepts it before closing. A signed document that can't be used is no solution at all.

This is why buyers need operational guidance, not just definitions. If you're planning a purchase from the United States, this 2026 guide to French property for US buyers gives broader context on how the remote process fits into the overall transaction.

What a French Power of Attorney Really Means

A power of attorney is a delegation, not a surrender of control. You remain the decision-maker. You authorize another person to perform defined acts in your place.

The U.S. Consumer Financial Protection Bureau puts the principle clearly in its guidance on what a power of attorney is. A POA can authorize an agent to help with banking, bill payment, taxes, or real estate, while still excluding acts the principal doesn't permit. The document itself sets the boundaries.

The two key French terms

For a French property transaction, you'll hear two words repeatedly:

Mandant means the principal. That's you, the person giving authority.

Mandataire means the agent. That's the person receiving authority to act for you.

A good way to think about it is this: you are not handing someone all your keys. You're handing over one specific key for one specific door, with clear instructions about what happens once they open it.

Why specificity matters

For a purchase in France, the notary usually wants a specific power of attorney, not a broad, generic document downloaded from the internet. In practice, that means the procuration should identify the property, the parties, and the legal acts to be signed.

That narrow drafting protects you in two ways:

It limits the agent's authority to the transaction you intend.

It reassures the notary and lender that the agent is acting within a clear mandate.

A broad POA from another jurisdiction may be legally valid where you live and still be operationally awkward in France. That's a frequent point of confusion in cross-border matters. If you want a useful common-law comparison, this resource on financial Power of Attorney in Ontario shows the same core principle: the document grants authority, but the wording controls the scope.

General and durable powers are not the same thing

This matters more for planning than for a straightforward purchase, but clients often ask. A durable POA remains effective after incapacity. A general POA may not. That difference is why durable powers are widely used in advance planning.

For a property signing, though, the main practical question is simpler: does the French notary have a properly drafted authority, acceptable in form, that allows the named person to sign the deed and any connected acts?

A power of attorney works best when it is narrow enough to be safe and detailed enough to be usable.

That balance is where experienced drafting matters.

Choosing the Right POA for Your Situation

French law offers more than one mandate structure, and non-resident buyers sometimes mix them up. For a property purchase, the wrong choice creates confusion at exactly the wrong moment.

The document most buyers need is the procuration. The document people often ask about, but usually don't need for closing, is the mandat de protection future.

The transactional option

A procuration is built for an immediate task. In property matters, it allows your agent to sign for you in a live transaction once the document is validly executed.

That's why it is the standard tool for a non-resident purchase. The notary can draft it around the actual file, the actual property, and the specific deed.

The advance-planning option

A mandat de protection future belongs to a different category. It is an incapacity-planning instrument. It must be put in place while the principal still has mental capacity, and if incapacity later occurs, the named mandataire must activate it through the local court with a medical certificate, as explained in this guidance on power of attorney in France.

That makes it useful for longer-term personal planning. It does not make it the normal document for signing a purchase deed next month.

Procuration vs. Mandat de Protection Future

Feature | Procuration (Standard POA) | Mandat de Protection Future (Future Protection Mandate) |

|---|---|---|

Main purpose | Authorises a specific person to act in a current transaction | Plans for future incapacity |

Typical property use | Signing a purchase deed or related notarial documents | Long-term estate and personal protection planning |

When it becomes effective | Used for the authorised act once validly signed | Not simply on signature alone in an incapacity scenario |

Capacity requirement at creation | Must be created by a capable principal | Must also be created while the principal has capacity |

Activation after incapacity | Not the main function of the document | Requires court activation and a medical certificate |

Fit for a live purchase closing | Usually yes | Usually no |

Which one actually works for a buyer abroad

If you are buying a flat in Paris, a chalet in the Alps, or a family home in Bordeaux and need someone to sign the acte de vente, the answer is almost always the same: use the procuration drafted by the French notary handling your sale.

Use the mandat de protection future if you are doing broader life and estate planning in France, especially where future incapacity is the concern. That is a separate discussion and often belongs in a wider family-asset strategy, not in the mechanics of a purchase closing.

A practical test

Ask one question: Am I solving a transaction problem or a future incapacity problem?

If the answer is “I need someone to sign my deed because I'm abroad,” you are almost certainly in procuration territory.

If the answer is “I want someone to manage my affairs later if I lose capacity,” you are in future-protection planning.

Buyers sometimes try to overcomplicate this because they've heard terms like “lasting power” or “durable power” in their home country. French notarial practice is more document-specific. The tool must match the job.

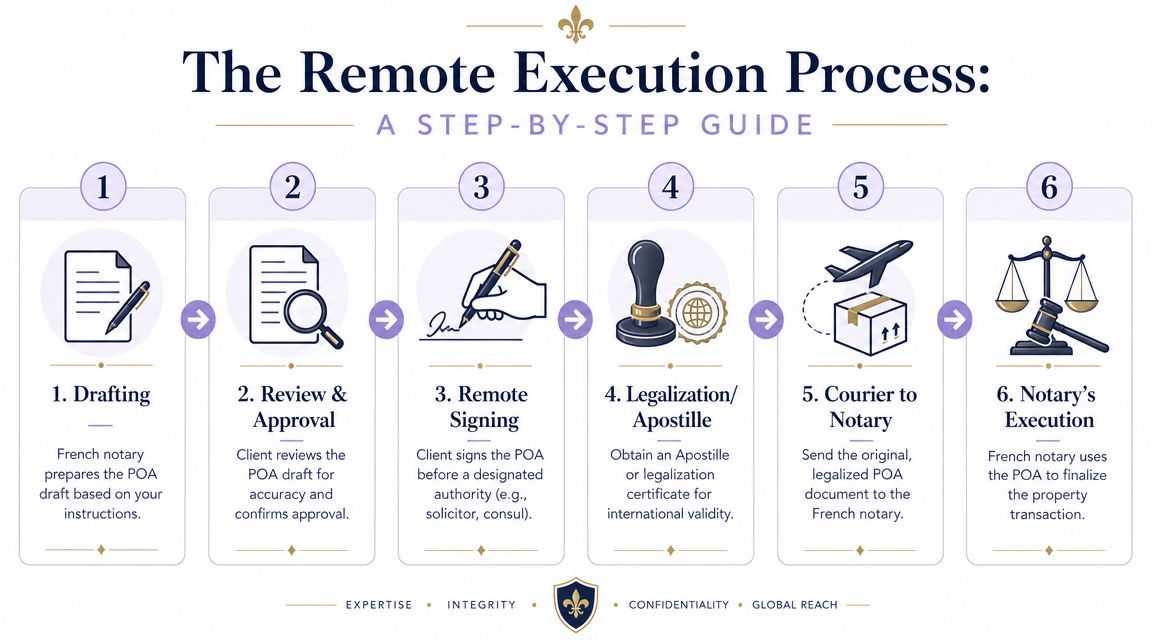

The Remote Execution Process A Step-by-Step Guide

When buyers say, “I'll just sign a POA abroad,” they often underestimate how formal the process can be. A French notary won't rely on improvisation. The document has to move through a sequence that preserves identity, authority, and legal acceptance.

Traditional route from abroad

The classic workflow usually looks like this:

Drafting by the French notary

The notary handling the property transaction prepares the procuration in the form required for that file.Review by the buyer

You check names, passport details, marital status if relevant, property description, and the scope of powers.Signature before a local authority

Depending on your jurisdiction and the notary's instructions, this may be before a local notary public, solicitor, or consular authority.Authentication

If required, the document then goes through apostille or legalization so it can be recognised in France.Translation if needed

If the French notary requires a French version or certified translation, that must be arranged before use.Delivery to the French notary

The notary typically wants the final document in time to verify it before signing day.

What works and what doesn't

What works is following the notary's drafting and signature instructions exactly. What doesn't work is using a generic template from another country and assuming France will accept it because it looks official.

The biggest mistake I see operationally is buyers trying to solve this too late. A POA is not difficult, but it is sequential. If one step slips, the rest slide with it.

Watch the details that trigger rejection

Pay close attention to:

Identity consistency. Your name must match your passport and the notary's file.

Property precision. The document should clearly tie back to the transaction it is meant to cover.

Authority wording. If the bank requires related mortgage signatures, the POA may need those powers expressly included.

Originals and timing. Some counterparties are comfortable with advance scans for review, but the notary may still require the final form before closing.

If the French notary drafts the wording, follow that version. Cross-border POAs fail more often from “helpful edits” than from legal complexity.

The newer remote notarial option

A major change improved life for non-residents. Since decree n° 2020-1422 of November 2020, French notaries can prepare authentic powers of attorney through remote appearance, as described in this overview of buying French property with power of attorney.

For the right file, that can remove the need for a foreign apostille because the document is handled through the French notary's authenticated remote process. Practically, this is often the cleanest route for buyers abroad who need speed and certainty.

It is not automatic in every case. The notary decides what is suitable, and the transaction type matters. But when available, it usually reduces friction dramatically.

If your circumstances are UK-based, this broader guide on how to invest in French property from the UK helps place the POA process within the wider financing and closing workflow.

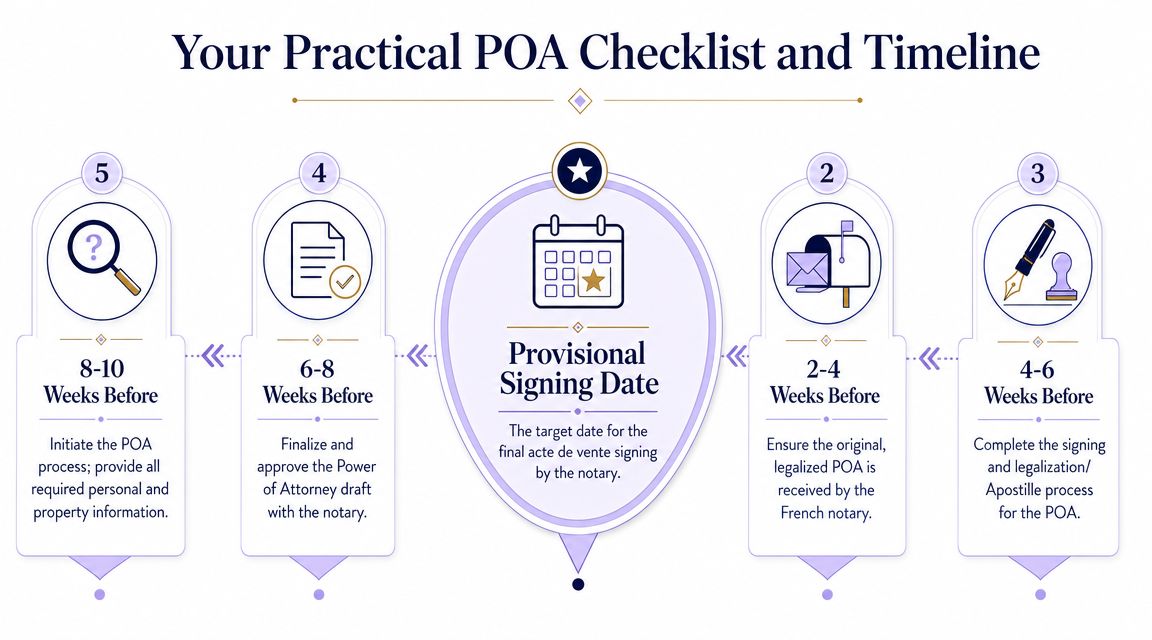

Your Practical POA Checklist and Timeline

The buyers who handle POAs calmly are usually the ones who start early. The buyers who panic are usually the ones who assume a notarised signature can be arranged in a day or two.

This reverse timeline is the one I recommend in practice. Use the signing date for the acte de vente as the fixed point and work backward.

Early stage preparation

Start with the signing date

As soon as the notary suggests a likely completion window, tell both the notary and your broker that you may need a procuration.Choose your mandataire carefully

This person needs to be trustworthy, reachable, and available on the actual day of signature.Provide full identification promptly

Delays often begin because the notary is still waiting for passport copies, civil-status details, or file information needed for drafting.

Draft and approval stage

Once the notary sends the draft, review it line by line. Don't skim. Check names, dates of birth, addresses, property references, and the exact act being signed.

A single mismatch can create avoidable back-and-forth at the worst possible time.

Questions to ask before you sign

Will this POA cover only the deed, or also loan-related documents?

Does the notary require an original hard copy?

Will apostille or legalization be necessary in my jurisdiction?

Is a French remote authentic POA available for my file instead?

The right time to ask acceptance questions is before signing the POA, not after couriering it.

Execution and delivery stage

After approval, move to execution without delay. If you are using the traditional route, book the signing appointment quickly and confirm the authentication process in your country. Then arrange any required translation and courier delivery.

If the file is suitable for remote authentic execution, the French notary usually coordinates the video-signing process directly. Even then, leave margin for technical scheduling and document checks.

A simple way to stay organised is to keep one checklist with five live items: draft approved, signature booked, authentication completed, translation completed if required, and final document received by the notary.

Common Pitfalls and How to Avoid Them

Most POA problems are not exotic legal failures. They are ordinary process mistakes. Buyers wait too long, use the wrong wording, or assume that any notarised document from abroad will be acceptable in France.

Pitfall one: starting too late

The hidden delay is rarely the signature itself. It is the chain after the signature. Authentication, translation, courier delivery, and notary review all take time.

The fix is simple. Raise the POA question as soon as the transaction begins to look real, not when the signing date is already approaching.

Pitfall two: using the wrong document

A generic foreign POA may be valid in your home system and still be unusable for a French property sale. French notarial practice is document-specific and transaction-specific.

Avoid that risk by using the French notary's draft. That gives the notary, the agent, and any connected lender a shared document built for the actual file.

Pitfall three: choosing the wrong agent

The legal point is trust. The practical point is reliability. Your agent must be someone who will answer messages, attend when needed, and follow instructions closely.

This is one of the few decisions in the process that the documents cannot solve for you.

A short risk-control list

Use the notary's wording instead of a template from the internet.

Check every personal detail against your passport and the sale file.

Confirm acceptance requirements in advance if the document is being signed outside France.

Pick an agent who is both trustworthy and available on the actual date.

Pitfall four: ignoring wider planning

A property procuration is transactional, but it often exposes a larger issue. Many people haven't arranged any broader decision-making authority at all. NIH StatPearls notes that advance-care-planning participation among U.S. adults has been reported in a range of 18% to 36% in studies it cites, which shows how often people lack a designated decision-maker before a crisis occurs, according to the StatPearls review.

That doesn't mean every property buyer needs a full incapacity-planning package immediately. It does mean the stress around one purchase often reveals a wider gap that should be addressed separately.

Next Steps with Your Broker and Notary

A French property purchase closes well when the broker, notary, and client are working from the same timeline. That's especially true if a lender is involved, because the POA may need to match both the property deed mechanics and the bank's documentary requirements.

Who should handle what

The notary should control the legal drafting of the procuration. Your broker should help coordinate timing with the financing file and flag whether related loan signatures may also need to be covered.

Your job is narrower but important. Review the draft carefully, appoint the right agent, and complete signature formalities quickly when the file is ready.

Practical support from your side of the border

If you need local signing support in a common-law jurisdiction, a service like Ontario notary support can help you understand the practical side of notarisation before documents go back to France. The key is always to confirm first that the French notary will accept the proposed route.

For buyers arranging the wider funding side remotely, financing French property for expats explains how mortgage coordination, document timing, and final signing fit together. In that context, Invexa is one example of a broker that works on remote non-resident French mortgage files and coordinates with notaries during closing.

The smoothest closing is usually the one where the POA is treated as part of the financing and notarial workflow from the start, not as a last-minute legal add-on.

Frequently Asked Questions About French POAs

A few final questions come up repeatedly once buyers understand the basics.

FAQ Table

Question | Answer |

|---|---|

Can I use a general POA from my home country to buy in France? | Sometimes a foreign document may be relevant, but for a French property transaction the safest route is usually the procuration drafted for the file by the French notary. Acceptance depends on form and wording, not just on whether the document is called a POA. |

Does a French property POA give my agent control over all my finances? | No. In a properly drafted transaction file, the authority is limited to the acts described in the document. |

Who should I appoint as mandataire? | Choose someone you trust completely and who can actually attend, respond quickly, and follow signing instructions. In practice, reliability matters as much as trust. |

Is the remote option always available? | Not always. It depends on the type of file and the notary's process. Ask early whether a remote authentic POA can be used. |

Do I still need to read the deed terms if someone else signs for me? | Yes. A POA changes who signs physically. It doesn't remove your responsibility to review the transaction you are authorising. |

What is the main mistake non-resident buyers make? | Leaving the POA discussion too late. Once the signing date is fixed, every missed day reduces your margin for corrections. |

If you're buying from abroad and want help coordinating the mortgage, notary timeline, and remote signing mechanics, Invexa can help you structure the process before it becomes urgent. That usually means identifying early whether a procuration will be needed, aligning it with the financing file, and keeping the closing on schedule.