Financial Stability Assessment: Expat Mortgage Guide

French expat mortgage application issues? Our guide details financial stability assessment criteria for expats & provides strategies to succeed.

published

Outrank AI

financial stability assessment, french mortgage, expat financing, non-resident mortgage, invexa

7707eaa3-4417-44a6-a2c0-a8901a9bb0d3

You've found the apartment in Paris, the chalet in the Alps, or the family house on the Atlantic coast. The seller accepts your offer. Then the true stress begins.

You live abroad. Your salary arrives in another currency. Your tax returns come from another country. Your bank statements don't look French. The bank isn't just asking whether you earn well. It's asking whether your finances will still hold together after exchange-rate moves, document delays, changing contracts, or a bad year in your business.

This is the core issue. A French lender runs a financial stability assessment, even if nobody uses that exact phrase on the first call. For an expatriate, this assessment is the difference between a file that looks strong on paper and a file a bank will finance.

The Expat's Dilemma Securing a French Mortgage

A non-resident mortgage file often looks better to the client than it looks to the bank.

I see this all the time. An expat says, “My income is high, I have savings, and I've never missed a payment.” All true. But the lender sees something else first: foreign income, multiple accounts, tax residence abroad, documents in different formats, and a loan that must be repaid in euros no matter what happens in your home country.

That gap creates frustration. You feel solvent. The bank feels uncertainty.

For South Africans in particular, tax status can complicate the file before the mortgage analysis even begins. If your residency position is still unclear, read this breakdown of Tax residency for South Africans. It helps clarify a point that French banks and insurers often scrutinize closely.

Why the process feels opaque

French lenders rarely reject an expat file because of one dramatic problem. They reject it because too many small uncertainties stack up.

Common examples include:

Income that is hard to classify: local salary, freelance revenue, dividends, retained profits, or offshore distributions

Debt that looks harmless to you but not to the bank: credit cards, personal loans, business guarantees, or family-related commitments

Missing local anchors: no French banking relationship, no euro reserves, no clear French tax angle

Documents that don't translate cleanly: foreign tax notices, company accounts, payslips, or proof of assets

Opening the right local account early can remove one layer of friction. If you haven't done that yet, start with this guide to opening a French bank account.

A French mortgage for a non-resident isn't blocked by complexity alone. It's blocked when complexity is left unexplained.

The good news is that the bank's logic is consistent. Once you understand how a lender judges stability, the process becomes far more manageable.

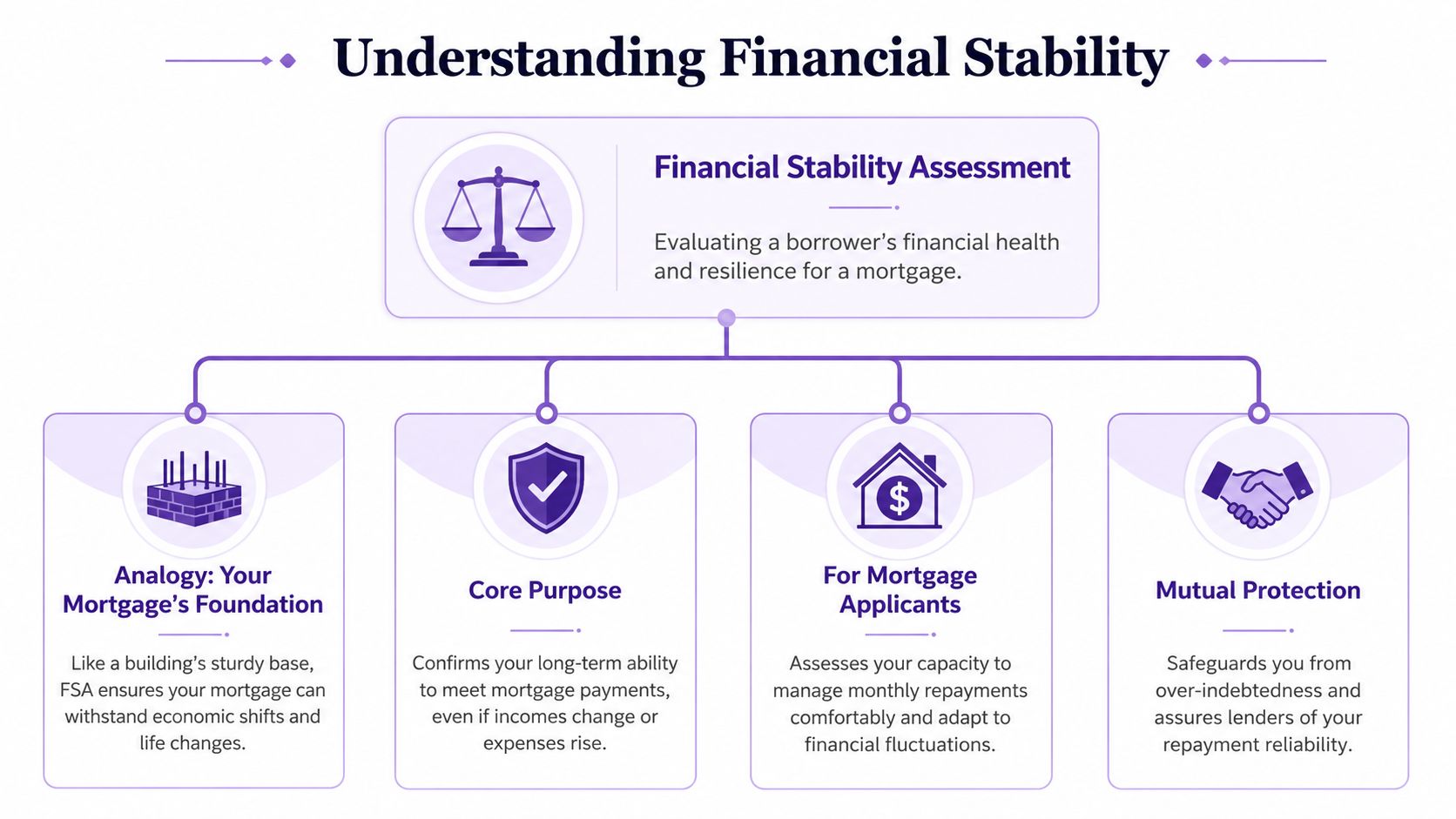

Understanding the Core Concept of Financial Stability

You can have a strong income, a healthy asset base, and still fail a French bank's stability test if your file does not prove one simple point. Your euro mortgage must remain affordable when real life gets less comfortable.

That is the core concept.

A financial stability assessment measures staying power, not just present-day income. For a non-resident borrower, the bank is not asking whether you can pay the first few instalments. It is asking whether your finances still hold if exchange rates move against you, bonus income drops, documents take longer to verify, or your employment structure looks less familiar from France.

What the bank is really testing

French lenders apply a practical standard. Can you service a euro-denominated debt through ordinary disruption without creating extra risk for the bank?

For an expatriate, that question becomes more demanding because the risk is rarely limited to one salary line. The bank often has to judge several moving parts at once:

Currency exposure: your income may be in dollars, pounds, dirhams, francs, or another currency, while the loan is in euros

Employment clarity: a foreign contract, self-employed structure, or company income can be acceptable, but only if it is easy to verify and consistent over time

Distance and administration: signatures, certified documents, tax returns, insurance paperwork, and bank statements take longer and create more room for doubt

Mixed income sources: salary, bonus, dividends, retained profits, rental income, or partnership draws do not carry the same weight in underwriting

The broader principle is well established. The IMF's Financial Sector Assessment Program, launched in 1999, was created to assess resilience to stress in financial systems, as noted in the IMF overview of the Financial Sector Assessment Program. The mortgage version is simpler but the logic is identical. Stability means resilience under pressure.

Why this matters more for expats

French banks are conservative. For non-residents, that is usually sensible.

A local salaried borrower gives the lender familiar reference points. A foreign borrower does not. Your employer may be unknown in France. Your tax documents may follow a format the underwriter never sees. Your income may be perfectly strong but harder to classify. As a result, the bank puts more weight on consistency, liquidity, debt burden, and document quality than many expats expect.

That is why presentation matters.

If your financial story needs context, provide the context before the underwriter asks. Do not send a pile of raw statements and hope someone at the bank will reconstruct your situation accurately. They will not. A good file explains where the income comes from, which part is fixed, which part is variable, what reserves you hold, what currency risk exists, and why the loan remains affordable under stricter assumptions. Debt capacity sits at the centre of that review, so it helps to understand the bank's method in Invexa's guide on French mortgage DTI.

Practical rule: If the underwriter has to guess, your file is already weaker than it should be.

What financial stability does and does not mean

Financial stability is wider than a credit score. It is wider than a salary multiple. It is also wider than net worth on paper.

A borrower with moderate but clean income, strong documentation, low existing debt, and meaningful euro savings can look safer than a high earner with offshore flows, irregular distributions, and no liquidity buffer in the right currency.

French banks reward clarity and predictability. Expats who understand that early put themselves in a much stronger position.

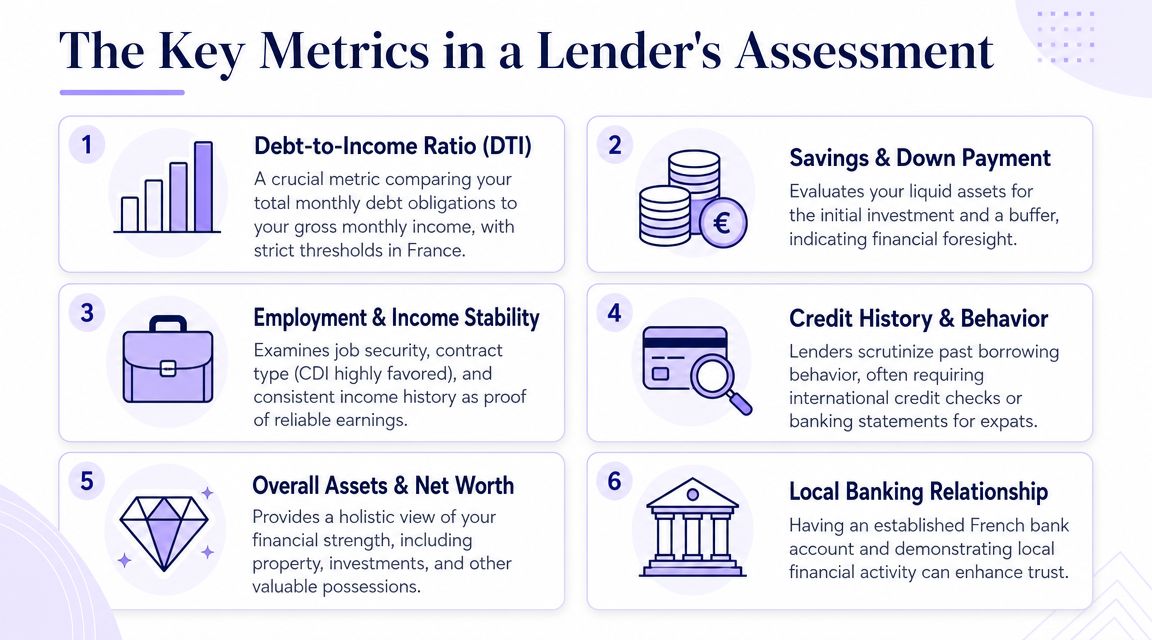

The Key Metrics in a Lender's Assessment

French banks do not assess non-residents emotionally. They assess them mechanically. If you know the mechanics, you can shape the file before submission instead of reacting after a refusal.

Income quality matters more than income size

A bank first wants to know whether your income is stable, understandable, and documentable.

Salaried income is usually the easiest to present, especially when the contract is long-term and the payslips are regular. Variable income is not impossible, but it needs work. Freelance revenue, company profits, performance bonuses, partnership draws, or offshore distributions create questions the bank will not ignore.

This is not a niche problem. A 2026 Cleveland Fed working paper noted that assessing resilience is complex for financially underserved groups, which can include people with cross-border, variable, or partly offshore income in the Cleveland Fed paper on trust among the financially underserved. That's exactly why a strong nominal income can still be judged unstable if the lender struggles to verify it or match it to the loan currency.

What banks prefer to see

Regular salary flows: monthly and traceable

Employment continuity: consistent role, sector, and employer history

Business clarity: if self-employed, clean company accounts and a clear extraction pattern

Document consistency: tax returns, statements, contracts, and payslips that tell the same story

Debt ratio is central, but not in isolation

French lenders care a great deal about your debt burden. They review existing obligations, not just the new French mortgage.

That includes:

Consumer debt: car finance, revolving credit, personal loans

Property debt: mortgages on homes abroad or buy-to-let assets

Support obligations: alimony or court-ordered payments where applicable

Business-linked exposure: sometimes guarantees or recurring commitments connected to your company

If you want the technical background, read Invexa's guide on French mortgage DTI. It explains why your own quick calculation often looks better than the bank's version.

Banks also adjust the quality of income, not just the amount. Foreign income may be weighted cautiously. Variable income may be averaged. Irregular dividends may be discounted. So two borrowers with the same headline earnings can produce very different lending outcomes.

Currency exposure can weaken a good file

In this situation, many expats lose credibility.

If you earn in a non-euro currency and borrow in euros, the bank has to consider mismatch risk. A salary that seems comfortable today can become tighter if exchange rates move against you. The lender may not describe this in detail, but it absolutely factors into the assessment.

A borrower looks stronger when they can show one or more of the following:

Risk area | What reassures the bank |

|---|---|

Income currency mismatch | A clear history of stable foreign earnings and thoughtful euro budgeting |

No euro reserves | Savings or investments already held in euros |

High dependence on bonuses | A file that remains affordable on base income or conservative assumptions |

Offshore business income | Full documentary trail and clean separation between company and personal finances |

A euro mortgage should be supported by a euro strategy, not by optimism about exchange rates.

Liquidity, assets, and down payment

Your cash position matters because banks don't just finance an acquisition. They assess your ability to absorb friction.

For an expat, liquidity answers several concerns at once:

Can you pay the down payment and costs without emptying your accounts?

Do you have a buffer after completion?

Are your assets liquid and accessible, or tied up in structures the bank can't rely on quickly?

Property wealth abroad can help your overall profile, but liquid savings usually speak louder than an illiquid asset portfolio.

Tax status, insurance, and structure

Tax residence affects both clarity and risk perception. If your declaration position is messy, the lender sees uncertainty. Clean tax filings matter.

Borrower insurance also matters more than many non-residents expect. French banks often treat insurance as part of the risk package, not as a separate afterthought. If your health history, country of residence, or profession complicates insurance, deal with it early.

Then there's the ownership structure. Sometimes borrowing personally is simplest. Sometimes an SCI can make sense, especially for family ownership, succession planning, or a shared investment strategy. But don't use an SCI just because someone online said it sounds impressive. Banks finance clarity, not decoration.

Preparing Your Financial Dossier for Success

A strong file is assembled, not improvised.

Most mortgage refusals for expats don't come from a lack of means. They come from a lack of structure. The lender wants a coherent picture, built from multiple inputs. That's normal. Even formal stability frameworks use dashboards rather than a single ratio. For example, the U.S. Office of Financial Research monitor uses 58 indicators across six categories, updated quarterly, to assess vulnerabilities through the OFR financial vulnerabilities framework. A French mortgage underwriter uses a different model, but the principle is identical. One number never tells the whole story.

What your dossier must include

Below is the minimum standard I recommend for an expatriate mortgage file.

Document Category | Specific Items Required |

|---|---|

Identity and residence | Passport, proof of current address abroad, residency permit if relevant |

Employment and income | Employment contract, recent payslips, employer letter if useful, bonus history if applicable |

Self-employed or business income | Company accounts, accountant letter, dividend records, salary slips, proof of ownership |

Tax documentation | Recent tax returns, tax assessments, proof of tax residence where available |

Banking evidence | Recent personal bank statements, statements showing salary credits, savings account statements |

Assets and savings | Investment statements, proof of liquid assets, evidence of down payment funds |

Existing debts | Mortgage statements, loan schedules, credit statements, monthly repayment evidence |

Property file | Signed offer or draft purchase agreement, property details, estimated costs |

Insurance and legal support | Existing life cover details if relevant, preliminary insurance information, power of attorney documents if needed |

Supporting explanations | Currency note, income summary, debt summary, brief memo explaining any unusual structure |

A simple example of how lenders read foreign income

Let's keep this practical.

Suppose you're paid abroad and want to know whether your debt ratio is acceptable. Don't just convert your salary into euros at today's rate and assume that's what the bank will use. The bank may take a more conservative view.

A simplified lender approach often looks like this:

Start with documented recurring income only.

Separate stable income from variable income.

Review the currency mismatch between income and the future mortgage.

Apply a cautious internal view to income that is volatile, hard to verify, or exposed to exchange-rate risk.

Add all existing monthly debt obligations before testing the new mortgage payment.

That is why your own spreadsheet can mislead you. You think you have plenty of room. The bank trims the usable income, keeps the debts at full value, and the ratio tightens quickly.

If you want a practical baseline before speaking to a broker or bank, use this framework for mortgage affordability for non-residents.

When income crosses borders, the issue isn't only how much you earn. It's how much the bank is willing to count.

Insurance preparation belongs in the dossier too. If you need to understand how lenders view pledged protection or related collateral concepts, this article on how to secure your loan with life insurance is a useful background read, especially for borrowers used to Anglo-Saxon lending structures.

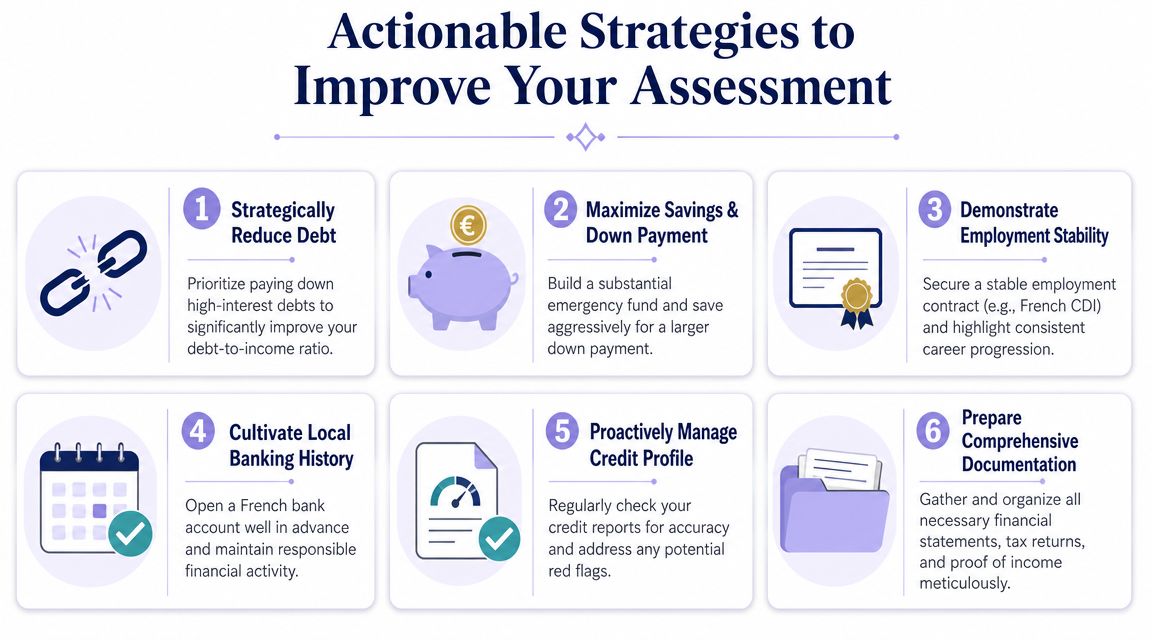

Actionable Strategies to Improve Your Assessment

You live abroad, earn in one currency, buy in another, and send documents from a distance. French banks will still approve the loan if your file answers three questions clearly: Is the income stable? Is the budget controlled? Can the borrower absorb a problem without missing payments?

Your job is to remove anything that makes the bank hesitate.

Remove the weak points first

Start with the elements that damage a French mortgage file fastest.

Clear short-term consumer debt: Revolving credit, personal loans, and car finance weigh heavily in underwriting. Paying them off often improves your assessment more than marginally improving your savings.

Keep part of your cash in euros: If the purchase, notary costs, and future repayments are in euros, banks want to see euro liquidity. Foreign savings still count, but euro reserves are easier for the lender to trust.

Show post-completion reserves: Do not drain every account into the deposit. A bank prefers a borrower who still has cash after signing.

Use one consistent document set: Same names, same dates, same currency logic, same totals across payslips, bank statements, tax returns, and asset summaries.

Distance creates friction. Poor formatting makes it worse.

Package foreign and variable income like an underwriter expects

Expats often lose points here. The issue is rarely income level alone. The issue is presentation.

If your earnings come from salary, bonus, dividends, freelance work, or a foreign company you own, separate each stream and document it on its own merits. Do not mix business turnover with personal income. Do not send raw statements and expect the bank to piece the story together.

A simple structure works well:

Situation | What the bank wants to see |

|---|---|

Bonus-heavy pay | Base salary identified clearly, bonus shown separately over time |

Self-employed or company owner income | Company accounts, tax filings, and the exact path from profit to personal income |

Offshore or foreign employer structure | A short written note explaining the employer, legal entity, contract type, and payment method |

Multiple currencies | Source currency, conversion method, and a clear plan for euro repayments |

For borrowers building clearer forecasts and cash-flow summaries, this guide to 9 steps for AI financial modelling can help you organize assumptions cleanly. The bank does not want a complex model. It wants a file that is easy to verify.

Use the improvements that matter most to French lenders

Do not waste time on cosmetic fixes. Banks respond to a short list of practical improvements.

A larger deposit helps because it lowers risk immediately. Stronger residual savings help because they show resilience after completion. Early insurance work helps because medical or residency questions can delay an otherwise acceptable case. A clean ownership setup helps too, but only after the financial basics are solid.

My recommended order is simple:

Reduce monthly debt pressure.

Separate and document income properly.

Increase euro liquidity and keep reserves after purchase.

Explain currency exposure and repayment strategy.

Resolve insurance questions early.

Only then consider structures such as co-borrowing arrangements or an SCI.

Borrowers abroad often try to compensate for a weak file with a more complex structure. French banks usually prefer the opposite. A simple acquisition with clear income, low debt pressure, and visible reserves will outperform a clever setup with unanswered questions.

Partnering with an Expert for a Seamless Process

An expat mortgage becomes difficult when nobody translates your reality into bank language.

That's where specialist support matters. You need someone who can read a foreign payslip, understand offshore or digital income, anticipate insurer questions, and package the file in the order a French lender expects. Otherwise, the bank sees complexity first and quality second.

A specialist broker also helps you avoid the usual timing mistakes. Expats often chase rates too early, insurance too late, and documentation in the wrong format. The better approach is the reverse: qualify the profile, validate the structure, prepare the file, target suitable banks, then move through approval and signing without constant rework.

If your income is foreign, your tax residence is outside France, or your project involves co-borrowing, an SCI, or non-standard assets, don't treat the mortgage like a domestic application. It isn't one.

Common Questions on Financial Stability for Expats

Does my high salary guarantee mortgage approval

No.

A high salary helps only if the bank considers it stable, verifiable, and compatible with a euro mortgage. Large income with weak documentation, strong currency mismatch, or heavy existing debt can still produce a poor assessment.

How do French banks view offshore company income

Carefully.

If you control the company, the lender will want to understand what belongs to the business and what is personal income. Clean accounts, a clear extraction method, and tax consistency matter more than ambitious revenue figures.

Is the financial stability assessment the same at every French bank

No, but the logic is similar.

The principles are broad and international. The IMF's Global Financial Stability Report assesses systemic issues, and monitoring approaches often span six broad areas, which shows how stability is judged through multiple lenses rather than one headline metric in the IMF's Global Financial Stability Report. French banks apply that mindset differently according to their own risk appetite, but they all care about resilience, clarity, and downside protection.

Can I borrow if my income is in another currency

Yes, often. But you must prove that the currency risk is manageable.

The strongest files show stable earnings, conservative affordability, and some practical planning around euro repayments. The weakest files rely on the assumption that exchange rates will stay favorable. A bank won't underwrite hope.

Do savings matter if my income is already strong

Yes.

Savings show that you can complete the purchase, absorb costs, and survive surprises without immediate stress. For an expat, liquidity also reassures the bank that distance and cross-border friction won't destabilize the loan after completion.

If you're buying property in France from abroad and want a clear answer on how a lender will view your profile, speak with Invexa. They work exclusively on French mortgages for expatriates and non-residents, and the first consultation is free and confidential.