Loan to Buy Property Abroad: The 2026 Expat Guide

Thinking of getting a loan to buy property abroad? Our 2026 guide for expats covers eligibility, documentation, lenders, and tax to help you secure financing.

published

Outrank AI

loan to buy property abroad, expat mortgage, international mortgage, buying property in france, non-resident financing

3ce460ac-bb7e-4d8c-9058-e0a7e5bea7bf

Buying abroad often starts the same way. You find the apartment in Paris, the villa in Portugal, or the family base in the south of France, and the property itself feels straightforward. Then the financing questions hit all at once. Which bank will even look at foreign income? How much cash do you need before a lender takes you seriously? Will your company structure help or hurt the file? And why does one adviser talk about tax, insurance, currency, and ownership structure before they even discuss rate?

That confusion is normal. A loan to buy property abroad is rarely blocked by one single issue. Files succeed or fail because the whole structure either makes sense to the lender or it doesn't. Non-resident borrowing is less about filling in forms and more about presenting a coherent risk profile across income, assets, residence, tax exposure, legal ownership, and documentation.

The buyers who move cleanly through underwriting usually do one thing early. They stop treating the mortgage as a separate task. The loan, the purchase structure, the source of funds, the currency path, and the notarial timeline all have to line up from the start. If one piece is weak, the rest of the file has to compensate.

Your Dream Home Abroad Starts Here

Most buyers arrive at this stage with a clear property goal and a blurry financing plan. That's backwards. The first real step isn't making an offer. It's checking whether your file can survive cross-border underwriting.

A lender looking at a non-resident borrower isn't just asking whether you can afford the property. They're asking whether they can verify your income, understand your legal and tax position, trace your funds, and enforce the loan cleanly if anything goes wrong. That is why overseas borrowing feels stricter than a domestic mortgage, even for financially strong applicants.

Start with the lender's version of your profile

Banks don't read your situation the way you do. You may see stable income, useful assets, and a sensible purchase. The bank sees a borrower paid in one country, taxed in another, buying in a third, possibly through a company or family structure, with documents in multiple languages.

That isn't a problem by itself. It just means the file has to be built in a way the underwriter can digest quickly.

The most useful early questions are practical:

Income clarity: Is your income salaried, self-employed, dividend-based, or mixed?

Residency position: Are you a resident abroad, recently relocated, or moving soon?

Ownership plan: Are you buying personally, jointly, or through a structure such as an SCI?

Funding path: Is your deposit already seasoned and accessible, or spread across accounts and entities?

Currency exposure: Will your income and mortgage sit in the same currency?

Practical rule: The stronger your file looks on paper, the less the bank worries about the parts it can't control across borders.

Buyers often spend too much time comparing rates before they know whether their file is bankable. In practice, the first win is getting your profile framed correctly. The rate conversation matters later. Structure comes first.

Initial Eligibility and Financial Reality Check

The first filter is simple. Do you have enough equity, enough documentable income, and a file that a foreign lender can verify without guessing?

For non-resident borrowing, the answer depends less on optimism and more on evidence. International lenders usually want a thicker cash cushion and a cleaner documentary trail than domestic lenders. According to International Citizens Insurance guidance on buying property abroad, expat mortgages may require 30% to 50% down, and buyers should also budget 10% to 20% of the purchase price for taxes, legal fees, and closing costs depending on the country.

That means the affordability question isn't only "Can you cover the monthly payment?" It's also "Can you fund the transaction without stretching your liquidity dangerously thin?"

What lenders test before they discuss terms

A non-resident bank file usually stands or falls on five points.

Deposit strength: Banks want to see that your contribution is available, traceable, and not being assembled at the last minute.

Income stability: Salaried income is usually the easiest to present. Self-employed and company-based income can work, but only if the accounts tell a consistent story.

Debt position: Existing mortgages, personal loans, and guarantees matter because the underwriter reads your global obligations, not just the new purchase.

Asset quality: Savings, brokerage accounts, retained earnings, and existing property can support the file if documented properly.

Residency coherence: A borrower with clear tax residence, address history, and banking patterns is easier to underwrite than someone with fragmented ties.

Your self-check before you approach lenders

Use this short screen before you start speaking to banks or brokers.

Area | What a lender wants to see |

|---|---|

Cash contribution | Funds are available, seasoned, and supported by statements |

Income | Stable source, clear contracts, tax returns, and continuity |

Credit profile | No unexplained arrears, defaults, or major gaps |

Existing commitments | Current liabilities clearly listed and supportable |

Purchase logic | Personal use, second home, or investment position explained consistently |

If you're buying a rental property, don't assume the deal will underwrite itself because the property could perform well. The financing case and the operating case are separate. If your plan includes short-term rental use, it helps to understand how lenders view hospitality-style income and what operators mean when they discuss secure STR funding, because property strategy often influences how you present the file, even when the mortgage itself relies primarily on personal income.

What works and what usually doesn't

Some patterns come up again and again.

What works

Clear salaried income with matching tax returns

Savings accumulated over time in personal accounts

A straightforward purchase in personal names

A co-borrower whose profile strengthens the file rather than complicates it

What usually doesn't

Last-minute transfers between countries with no explanation

Offshore company income with weak personal extraction records

A mismatch between declared residence and actual banking activity

Trying to solve affordability with projected rent instead of provable income

Buyers looking at France should spend a little time on understanding French property mortgage mechanics before setting a budget, because the lender's affordability model can differ sharply from what feels comfortable on a spreadsheet at home.

A good file doesn't hide complexity. It organizes it.

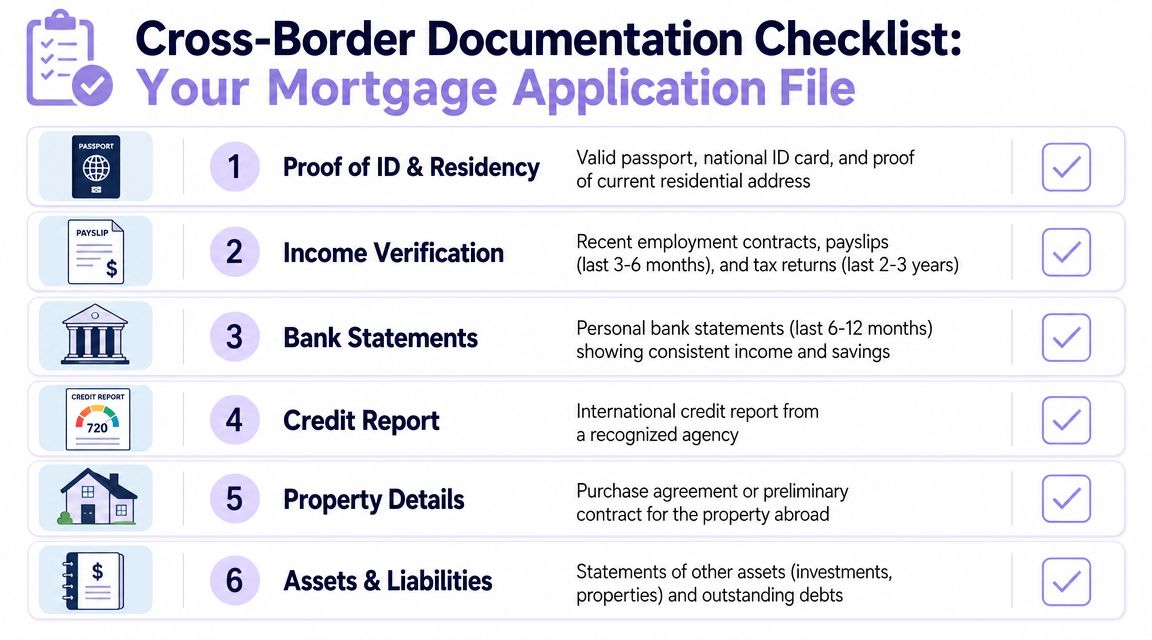

Assembling Your Cross-Border Documentation

A non-resident mortgage file succeeds or fails before underwriting starts. I see this constantly. The borrower may have strong income and a healthy deposit, but the file is built like a stack of disconnected documents instead of a credit case.

Cross-border lending is less about collecting paperwork than about structuring evidence. The bank needs to see how income is earned, where money accumulates, which country taxes it, and who will hold the property. If those points sit in separate folders without a clear link between them, the underwriter starts asking basic questions late in the process. That is where delays, repricing, and avoidable declines begin.

Build one credit story, not four separate files

Non-resident applications often involve four parallel realities. Personal income. Business income. Assets held in another country. A purchase taking place under a different legal and tax system. The job is to make those realities line up.

A lender will usually work with complexity if the structure is logical and documented early. Foreign salary can be bankable. Dividend income can be bankable. Retained profits, trust distributions, and income drawn from an offshore company can also work in some cases. What weakens the file is poor sequencing. For example, if tax returns show one pattern, bank statements show another, and the purchase will be made through an SCI or other vehicle that was only mentioned after the agreement was signed, the underwriter has to rebuild the case from scratch.

That is avoidable.

What the document pack needs to prove

The strongest file answers five questions in order.

Who is borrowing?

Passport, proof of address, visa or residency documents if relevant, and tax residence evidence should all match the same current profile.How is income generated?

Salaried applicants need contracts, payslips, and tax returns that reconcile cleanly. Business owners usually need company accounts, personal returns, dividend vouchers, accountant confirmation, and a clear explanation of how profits become personal income.Where did the deposit come from?

Savings history matters more than the headline balance. Large recent transfers, crypto liquidation, family gifts, or proceeds routed through multiple jurisdictions often need a paper trail before a bank asks for it.What obligations already exist?

Existing mortgages, maintenance payments, credit lines, and business guarantees affect affordability and risk. Declare them early.How will the property be owned?

Personal ownership, joint ownership, or an SCI can each be workable, but the documents must match the legal route from the start. Ownership structure is not an administrative detail. It shapes underwriting, notary work, insurance, and sometimes tax treatment.

Currency, tax, and legal structure belong in the file from day one

This is the part many borrowers leave too late.

If income is in dollars, sterling, dirhams, or Hong Kong dollars and the loan will be in euros, the underwriter will not look at income in isolation. They will look at exchange-rate exposure, the consistency of earnings in the source currency, and whether the borrower still passes affordability after the bank applies its own haircut or conversion method. A file that explains the currency position clearly is easier to defend than one that leaves the lender to make assumptions.

The same applies to tax. A borrower paid through a foreign company may look strong on gross earnings and weak on taxable personal income. An expat with multiple residencies may have a perfectly legitimate setup that still appears inconsistent if the tax documents are incomplete. The fix is usually simple. Add a short explanation, supported by returns and accountant evidence, showing where tax is paid and how income flows to the borrower.

Legal structure matters just as much. If you intend to buy through an SCI, set that up early with advice from the notary and tax adviser, then present the mortgage file on that basis. Changing from personal ownership to an SCI halfway through often triggers fresh underwriting questions, revised documents, and delays at exactly the wrong moment.

Practical points that save time

Translations should be done before submission, not after first review. Dates, names, and address formats should match across documents. If an employer letter uses one compensation figure and the payslips show another because of bonuses, allowances, or housing benefits, explain it in writing. If funds moved between personal and company accounts for legitimate reasons, label that trail before the bank asks.

One concise cover note can save weeks. I often structure it around income, assets, liabilities, residence, and ownership route so the underwriter can verify the logic quickly.

If you will not be present for every signing step, review how a French property POA for non-residents works early in the process. Power of attorney is useful only if the lender, notary, and transaction timetable are aligned before documents are issued.

Choosing Your Lender and Loan Structure

A non-resident mortgage file is won or lost at the structuring stage. I see borrowers spend weeks collecting documents, then hit avoidable resistance because the lender was wrong for their income profile, or the ownership route was chosen too late.

A bank is not only pricing risk. It is deciding whether your income, deposit, tax position, and legal structure fit its credit policy in a form the underwriter can sign off without hesitation.

Match the lender to the file, not the other way round

Buyers usually consider three routes. A local bank in the country of purchase, a lender in their country of residence with international capacity, or financing raised against an existing home.

The right option depends on where the file is strongest.

Option | Usually strongest for | Main trade-off |

|---|---|---|

Local bank | Buyers whose income and purchase logic can be explained clearly in the property's country | More local documentation, more scrutiny on translations, and less flexibility for unusual foreign income |

Overseas lender | Borrowers with straightforward salaried income and a simple ownership plan | Fewer solutions for country-specific legal structures or mixed income sources |

Equity release | Owners with substantial equity at home who want to avoid foreign mortgage underwriting limits | Your existing home carries the debt risk, and the structure can become less efficient from a cash flow or tax angle |

In practice, the cheapest rate is not always the strongest choice. A lender with a slightly higher margin but a credit policy that accepts foreign bonus income, offshore dividends, or non-resident co-borrowers can be the safer route to approval.

Loan structure starts with the underwriter's questions

Underwriters reviewing non-resident files focus on a short list of pressure points. If those points are addressed early, the case usually moves well. If they are left until the bank asks, the file slows down.

Currency alignment

If income comes in dollars, pounds, dirhams, or Swiss francs and the loan is in euros, the lender will test resilience, not just affordability on today's rate. Some banks apply internal haircuts to foreign income. Others want more surplus income after existing liabilities. A few will reduce the maximum loan amount without saying so directly.

That changes strategy. Sometimes the answer is a lower loan-to-value ratio. Sometimes it is choosing a lender comfortable with the income currency. Sometimes it means keeping more post-completion liquidity visible in the file.

Tax position

For non-residents, tax is part of credit analysis, not a side issue for later. The bank wants to understand where income is taxed, what reaches your personal account, and whether the ownership route creates a different tax treatment after completion. Buyers considering rental use should review likely charges early, including 2025 non-resident property tax rates, because net affordability can look different once local taxation is factored in properly.

A file reads better when the tax logic matches the borrowing logic.

Legal ownership structure

Personal ownership is usually easier to underwrite. Buying through an SCI, a family vehicle, or another holding structure can still work well, but only if the reason is clear from the start. The bank may ask who owns the shares, who gives the guarantee, who services the debt, and whether personal income supports the company sufficiently.

An SCI should solve a real succession, governance, or co-ownership issue. It should not be added because it sounds advanced.

I have seen good borrowers weaken their case by presenting an SCI with no clear explanation, or by switching from personal ownership to an SCI after the approval in principle. That often reopens underwriting, changes the required documents, and can affect the lender's security package.

Build the structure around the full profile

Expat files differ from domestic applications. Foreign salary, retained company profits, offshore entities, split tax residence history, and future family ownership plans all interact. Treated separately, they look messy. Presented as one coherent structure, they often become underwritable.

A specialist broker can help decide whether the loan should sit in personal names, whether an SCI belongs in the file from day one, and which lender will read foreign income in the most practical way. For example, Invexa handles remote mortgage applications for expatriates and non-residents buying in France, including cases involving foreign income, borrower insurance, and SCI structuring. That support matters most when the borrower is financeable but the file needs to be assembled in a way the right bank will approve.

Navigating Currency, Tax, and Insurance

Buyers often underestimate the total cost of buying abroad. They secure a mortgage in principle, feel relieved, and then discover that currency movement, tax treatment, and insurance conditions have more impact on day-to-day affordability than they expected.

The issue isn't that these topics are obscure. It's that they sit across different advisers. The bank discusses lending. The notary focuses on transfer. The accountant looks at tax. The insurer reviews health, age, residence, and coverage terms. If nobody coordinates them, you end up with a mortgage that works technically but not comfortably.

A typical sequence in the real world

A salaried expat often starts with a simple assumption. Salary is stable, the employer is known, and the property will be used part time. On paper, the loan looks uncomplicated.

Then the practical layers appear. The deposit may sit partly in one currency and partly in another. The tax residence may be clear personally but less clear for bonus income. The insurance questionnaire may take longer than expected because medical history, residence country, and planned coverage all affect the underwriting path.

An entrepreneur sees a different version of the same problem. The business may be profitable, but profits retained in a company don't always help if the bank wants proof of personal income extraction. Add a company structure, foreign dividends, and a purchase through a holding vehicle, and the file stops being a pure mortgage file. It becomes a legal and tax package.

The three issues to settle early

Currency management: Match income and debt where possible, or leave enough cash buffer that exchange movements don't create stress.

Tax visibility: Make sure declared income, tax residence, and ownership structure don't contradict each other.

Borrower insurance: Treat insurance as part of approval, not an afterthought. If the insurer asks extra questions, the credit timeline can move with it.

Buyers of French property should also review the local tax picture early. A practical starting point is this guide to 2025 non-resident property tax rates, because ownership cost isn't only about the loan. It also affects how you choose between personal ownership, co-ownership, and a more formal structure.

The cleanest transactions are the ones where the bank, notary, insurer, and tax adviser are all working from the same version of the deal.

The Application Timeline and Real-World Examples

Cross-border financing works better when you expect an underwriting process, not a quick approval. The practical workflow usually starts by comparing home-country and destination-country lenders, then obtaining an agreement in principle, assembling identity, income, and residency documents, and only then submitting the full mortgage file, as noted in Wise's overview of overseas property loan steps.

A realistic sequence

Most successful files follow a recognizable pattern, even if the exact dates vary.

Early review of profile

Before making the purchase fully real, the borrower checks lender appetite, ownership plan, and source of funds.Agreement in principle

This isn't final approval. It is a useful signal that the file is plausible in its current form.Document build

Income, address, residency, asset, liability, and purchase papers are assembled and standardized.Full underwriting

The bank reviews the borrower and property together. Questions usually arrive here, not before.Offer and conditions

Insurance, final signatures, and any legal-structure confirmations are aligned.Completion with notary and fund release At this stage, good planning pays off. Last-minute friction usually comes from missing documents or inconsistent versions of the file.

Example one, salaried expat buyer

A US citizen on a local employment contract wants to buy a Paris flat as a medium-term residence and family base. Income is easy to explain. The problem is not salary. The problem is presentation.

The buyer initially sends payslips, a contract, a US credit file, and a French purchase agreement. Individually, each document is fine. Together, they leave questions about tax residence, bonus treatment, and how the deposit moved from US savings into a European account.

Once the file is reorganized around current residence, employer continuity, and source of funds, the lender's objections shrink quickly. This is common. The borrower was bankable from the start. The first version of the file made the underwriter work too hard.

Example two, international entrepreneur

A digital entrepreneur wants to buy a second home in Provence. Revenue comes from multiple jurisdictions, business income sits partly inside a company, and personal salary is modest compared with overall wealth.

This type of borrower often assumes net worth will carry the file. It usually doesn't. The lender wants to know what income is personal, recurring, taxable, and available for repayment. The bank also wants the ownership choice settled early. Personal purchase and company-linked purchase are not interchangeable in underwriting.

What works here is disciplined separation. Company accounts show business health. Personal accounts show extraction and liquidity. The purchase structure is justified in legal and tax terms, not improvised late in the process.

A lender can accept a complicated profile. It rarely accepts a confusing one.

Expert Answers to Your Top Questions

Some questions come up in almost every non-resident purchase. The answers are rarely one-word yes or no.

Many buyers also assume rental yield will help carry the application. In reality, projected rent often does less than expected. Simon Conn notes in its buying property abroad FAQs that in most instances rental income cannot be used in mortgage calculations, and lenders typically rely on earned, pension, and sometimes investment income.

Frequently Asked Questions

Question | Answer |

|---|---|

Can I get a loan to buy property abroad if I'm paid in a foreign currency? | Yes, often you can. The key issue is whether the lender can verify the income, understand its stability, and get comfortable with the currency mismatch. |

Will projected rental income help me borrow more? | Usually not in the way buyers expect. Many lenders focus on earned, pension, and sometimes investment income rather than future rent. |

Should I buy personally or through an SCI or company? | It depends on your tax, succession, and family objectives. The wrong structure can complicate approval, so the mortgage and ownership plan should be designed together. |

Is a bigger deposit always the best solution? | Not always. More equity can help, but it won't fix unclear income, weak documentation, or a contradictory legal structure. |

Can I apply directly to banks instead of using a broker? | Yes. Direct applications can work for straightforward files. A broker becomes useful when income, residence, currency, or ownership structure needs to be matched to the right lender. |

If you're buying in France from abroad, the practical advantage comes from getting the file structured before it reaches underwriting. Invexa works specifically on French real estate financing for expatriates and non-residents, including foreign income cases, co-borrowing, SCI-related projects, and remote applications through to notary signing. If your profile is simple, that preparation keeps the process efficient. If your profile is complex, it can be the difference between a plausible project and a financeable one.